Abstract

Interest in the drivers of firms’ corporate social responsibility (CSR) is growing. However, little is known about the influence of a CEO’s childhood experience of natural disasters on CSR. Using archival data, we explore this relationship by offering three mechanisms that may account for how the CEO’s childhood experience of natural disaster is related to their CSR. More specifically, while prior research has established a positive relationship based on the post-traumatic growth theory, we show that the dual mechanisms of prosocial values and a CEO’s risk aversion explain the positive relationship. We further find that the positive relationship is stronger (1) when CEOs have longer career horizons and (2) when community social capital is high. This study contributes to both research and managerial implications on the topics of CEO’s childhood experience and CSR. In particular, this study advances the upper echelon theory by revealing that a CEO’s childhood experience of natural disaster is a useful yet relatively underexplored variable that can help explain the substantial variations in firms’ CSR. Moreover, we emphasize that a CEO’s career horizons and level of community social capital are important variables that further amplify the effect of a CEO’s childhood experience of natural disaster on the firm’s CSR commitment.

Similar content being viewed by others

Introduction

CSR has garnered a great deal of attention globally over the past few decades due to stakeholder pressures (e.g., Helmig et al., 2016; Perez-Batres et al., 2012) and as a means to enhance competitive advantage, corporate image, customer satisfaction (Saeidi et al., 2015), and ultimately financial performance (Flammer, 2015). Although various efforts have been made to understand the drivers of a firm’s CSR commitment, relatively few studies have focused on the influence of the CEO (Al-Shammari et al., 2019; Yuan et al., 2019) as opposed to firm- and institutional-level determinants. According to upper echelons theory, heterogeneities in corporate actions and outcomes are the result of differences among corporate executives (Hambrick & Mason, 1984) who have various values, motivations, psychological beliefs, personalities, demographic characteristics, and personal experiences that often inform their corporate decisions (Cox & Cooper, 1989). Quigley and Hambrick (2015) note the emergence of a CEO effect in which the proportion of variance in corporate decisions is increasingly explained by individual CEOs over the past few decades compared to earlier postwar decades, emphasizing the significance of understanding CEOs at an individual level to predict firm performance.

As a public firm’s most powerful figure, the CEO exerts considerable discretionary power in making a firm’s strategic decisions (Hambrick and Mason, 1984). Therefore, the role of the CEO is crucial in predicting a firm’s commitment to CSR (Chen et al., 2019; Orlitzky et al., 2017; Yuan et al., 2019). In recent years, proponents of the upper echelons theory have begun to explore the influence of CEO characteristics on a firm’s CSR performance (e.g., Chen et al., 2019; Yuan et al., 2019), including demographics (Dadanlar & Abebe, 2020; Lei et al., 2021; Oh et al., 2016; Papadakis, 2006), personality (Al-Shammari et al., 2019; Petrenko et al., 2016), values (Chin et al., 2013; Zhang et al., 2021), and motivations (Boone et al., 2020). Some of these have explored the CEO’s life experiences in connection with the CSR, but the primary focus has been placed on career experiences in adulthood (Chen et al., 2019; Slater & Dixon-Fowler, 2009).

However, limited research has focused on the role of the CEO’s off-the-job (Wang & Yan, 2022) and non-work-related (Tian et al., 2022) childhood experiences, including natural disaster, on a firm’s strategic decisions such as CSR. This is surprising because children’s experiences with adverse or traumatic events can “plant the seeds for far-reaching physical, cognitive, and emotional changes” (Peek et al., 2018, p. 243), consistent with the premise of the imprinting theory that emphasizes how the imprints of experiences during sensitive periods characterized by short time windows persist, despite subsequent environmental changes (Marquis & Tilcsik, 2013). Moreover, since a CEO’s off-the-job and non-work-related experiences are independent of the firm’s characteristics, they can readily facilitate the identification of the CEO’s managerial decisions (Wang & Yan, 2022).

Notably, O’Sullivan et al. (2021) have begun this conversation in a recent study by establishing a positive relationship between the CEO’s early-life disaster experience and CSR. They made an important initial step by relying on the post-traumatic growth theory as a theoretical anchor, arguing that CEOs who dealt with traumatic early-life events gain psychological strength from such experiences and that their psychological growth informs firm conduct. In line with their research, we borrow three other mechanisms (i.e., prosocial values, risk-aversive, and risk-taking tendencies) from the psychology and finance literature that might also explain this relationship and propose competing hypotheses that suggest a positive and a negative relationship between the CEO’s childhood experience of natural disaster and CSR.

Even if post-traumatic growth theory is useful to explain how individuals who experience traumatic events develop more positive psychological growth, O’Sullivan et al. (2021) did not consider the unique characteristics of natural disaster experiences through which victims develop prosocial values leading to altruistic behaviors such as CSR activities (e.g., Maki et al., 2019; Oishi et al., 2017), which we employed as one of the mechanisms. Moreover, while existing literature predominantly views individuals’ risk preferences (i.e., risk-aversive and risk-taking) formed by the natural disaster experience as key mechanisms in understanding the influence of natural disaster experience on strategic decisions, O’Sullivan et al. (2021) only acknowledged the potential risk-taking mechanism and controlled for it to partial out its effect on CSR. They did not test the risk-taking tendency as a mechanism in their analysis. To extend our knowledge, we elaborate on the influence of a CEO’s childhood natural disaster experience on their individual risk preferences as mechanisms and conduct relevant empirical testing and analyses. Thus, we attempt to unpack other mechanisms than post-traumatic growth through which CEOs with childhood natural disaster might or might not engage in CSR.

Taken together, we investigate three mechanisms (i.e., prosocial values, risk-aversive, and risk-taking tendencies) on the influence of the CEO’s childhood natural disaster experience on CSR and explore one CEO-level factor (i.e., CEO career horizons) and one community-level factor (i.e., community social capital) as two important moderators. We test our research proposal using a sample of 739 U.S.-born CEOs from S&P 1500 companies with 3,970 firm-year data spanning 2001 to 2013. Integrating the three mechanisms offers a comprehensive understanding of the relationship between the CEO’s childhood experience of natural disaster and CSR. Given the complex nature of the psychological impact of the childhood natural disaster experience as well as the risk preferences developed by the experience, it is imperative to embrace these perspectives across the disciplines and examine the explanatory power of them. Moreover, by acknowledging how this relationship strengthens under the two conditions of CEOs with longer career horizons and high levels of community social capital, this study emphasizes the variations of the individual reactions to the similar experience.

This study makes important contributions to the literature. First, this study enriches the research on upper echelons theory and extends our understanding of the relationship between the CEO’s characteristics and the firm’s commitment to CSR (Al-Shammari et al., 2019; Chen et al., 2019; Gröschl et al., 2019; Petrenko et al., 2016; Slater & Dixon-Fowler, 2009; Waldman et al., 2006; Yuan et al., 2019). To complement and extend the findings of O’Sullivan et al. (2021), who pioneered the investigation of the relationship between CEO’s early-life disaster experience and CSR, the current study promotes a profound understanding of the phenomenon by exploring three additional explanations (i.e., prosocial values, risk-aversive, and risk-taking tendencies) and delving into a CEO’s career horizon and community social capital as potential boundary conditions.

Second, our study adds to the strategic management literature by introducing the insight of imprinting theory. Although a CEO’s childhood experience of natural disaster occurs decades before they enter the corporate world, our results demonstrate that the imprinting effect of the experience persists in the CEO’s strategic decisions made in adulthood. Guided by imprinting theory (Marquis & Tilcsik, 2013), we offer concrete evidence pointing to a CEO’s childhood natural disaster experience as a source of imprinting that informs a firm’s engagement in CSR.

Finally, we extend the literature related to the corporate outcomes for CEOs with childhood natural disaster experience. While previous research tends to focus on corporate-level financial policies (Bernile et al., 2017; Chen et al., 2021; Dessaint & Matray, 2017; Yao et al., 2020), innovation (Chen et al., 2022), and COVID-19 crisis management (Ru et al., 2022), our findings demonstrate that a CEO’s childhood natural disaster experience positively affects their CSR decisions. Therefore, this study contributes to the CSR literature by identifying CEO’s childhood natural disaster experience as an antecedent of a firm’s CSR activities.

Related Literature and Empirical Predictions

The Childhood Experience of Natural Disaster and Imprinting Theory

Natural disasters are often considered a threat or a crisis (Hale et al., 2005). As common phenomena that affect nearly 160 million individuals worldwide every year (Institute for Economics & Peace, 2020), natural disasters including earthquakes, droughts, landslides, floods, hurricanes, and tornadoes are physical events that create a rapid and damaging socioeconomic impact, leading to the immediate need for external assistance to the population affected (North & Hong, 2000).

Most existing research in the domain of business has studied the impact of natural disasters on individual- or household-level risk-taking or aversion behaviors, including household investment in risky financial assets (Balasubramaniam, 2021), investment portfolio volatility (Bernile et al., 2021), and the purchase of flood (Gallagher, 2014), life (Gao et al., 2020), or home insurance (Wang et al., 2012). For instance, Wang et al. (2012) find that those who experienced significant damage to their homes or property due to natural disasters are more likely to accept disaster home insurance, while those who only perceived the threat are less likely to do so. Similarly, Shupp et al. (2017) show that victims who were directly impacted (i.e., injured) by a tornado have increased risk aversion as measured using a number of safe choices made by the participants in the assigned task, while those who were indirectly impacted (i.e., lost a friend or neighbor) have reduced risk aversion.

While these studies shed light on the role a natural disaster experience plays, questions remain about the long-term effects of experiencing a natural disaster in early life or childhood. Children, generally viewed as those below the age of 12 years (Office of Disease Prevention & Health Promotion, 2020), are a “vulnerable population at risk” (Landrigan, 2004, p. 175), often grouped with females, racial or ethnic minorities, the elderly, and those with disabilities (Peek et al., 2018; Rubin et al., 2019). Considering children’s lack of cognitive and emotional capabilities to cope with disaster as well as their rapid physical, cognitive, and emotional development, the importance of understanding the influences of the childhood experience of natural disaster has been highlighted as a meaningful avenue for investigation (e.g., Masten & Narayan, 2012; Peek et al., 2018).

Imprinting theory offers guidance in this quest. This theory highlights the existence of sensitive periods in which individuals “develop characteristics that reflect prominent features of the environment, and these characteristics continue to persist despite significant environmental changes in subsequent periods” (Marquis & Tilcsik, 2013, p. 199). These sensitive periods are characterized by a short and limited time window and are known to have more significant impacts on individuals than normal times (Immelmann, 1975), including childhood (Han et al., 2022; Kish-Gephart & Campbell, 2015), early career stages (Dobrev & Merluzzi, 2018; McEvily et al., 2012), and the early twenties (Zhang et al., 2022b).

Previous research has provided suggestive evidence that early exposure to natural disasters in childhood could lead to long-lasting cognitive, emotional, and physical impacts that may not be revealed for decades (Osofsky et al., 2015; Rubin et al., 2019). In the disaster literature, some evidence suggests that exposure to traumatic events such as war at a young age has a lasting impact on the victim’s life, even as long as five decades later (Choi & Jung, 2021; Kim & Lee, 2014). Recent findings in this line of research in business also strongly favor the long-lasting effect of natural disasters experienced by CEOs in childhood, as manifested in subsequent corporate-level decisions made later in their life (e.g., Bernile et al., 2017; Chen et al., 2021; Ru et al., 2022; Yao et al., 2020). However, since these studies largely focused on a firm’s financial policies rather than CSR as a likely outcome, it is important to explore what explains the relationship between CEOs’ childhood natural disaster experience and a firm’s CSR performance and what boundary conditions might exist.

Determinants of CSR and Upper Echelons Theory

CSR refers to “a discretionary allocation of corporate resources toward improving social welfare that serves as a means of enhancing relationships with key stakeholders” (Barnett, 2007, p. 801). Much of the prior research emphasizing the importance of engaging in CSR activities has focused on the relationship between CSR and corporate financial performance (e.g., Ruf et al., 2001; Shin et al., 2018). In a meta-analysis of the link between CSR and corporate financial performance, CSR is found to enhance a firm’s reputation, reciprocation of external stakeholders, and innovation capacity while it decreases firm risk, which eventually leads to improved corporate financial performance (Vishwanathan et al., 2020).

To explain the substantial differences in firms’ CSR performance, theorists have mainly examined externally driven determinants, such as government requirements (e.g., Vallentin, 2015) and institutional pressures, particularly from stakeholders (e.g., Helmig et al., 2016; Perez-Batres et al., 2012). They have studied the within-firm determinants of CSR relatively less (Al-Shammari et al., 2019; Chin et al., 2013). More recently, researchers have recognized that a firm’s decision to engage in CSR may depend on the preferences and priorities of the CEO as well as the top management team (e.g., Liu et al., 2017; Petrenko et al., 2016; Sajko et al., 2021). This view draws on upper echelons theory, which posits that CEOs’ personal characteristics are important drivers of firms’ strategies and performance (Hambrick & Mason, 1984). Aspects of CEOs increasingly explain a substantial portion of the variance in firm performance (Quigley & Hambrick, 2015). CEOs, as the top decision-makers of a company, hold substantial authority and control over firm strategies and resource allocation (Papadakis, 2006). Therefore, it is vital to understand the role of the CEO in a firm’s CSR performance (Chen et al., 2019; Orlitzky et al., 2017).

Most researchers who have explored the role of the CEO in the context of a firm’s CSR performance have narrowly attributed the determinants of CSR to the CEO’s demographic characteristics, such as age (Huang et al., 2012; Oh et al., 2016), education (Papadakis, 2006), gender (Dadanlar & Abebe, 2020), and geographical birthplace (Lei et al., 2021); psychological characteristics, including personality traits such as overconfidence (McCarthy et al., 2017), narcissism (Al-Shammari et al., 2019; Petrenko et al., 2016; Tang et al., 2018), materialism (Davidson et al., 2019), and hubris (Tang et al., 2018); values such as political ideologies (Chin et al., 2013; Gupta et al., 2021); motivations such as intrinsic and extrinsic motivations (Boone et al., 2020) and greed (Sajko et al., 2021); and career-related experiences, such as tenure (Chen et al., 2019; Finkelstein & Hambrick, 1990), military (Nasih et al., 2019; Zhang et al., 2022b), and overseas work experiences (Slater & Dixon-Fowler, 2009) obtained in the adult stage. Most recently, Wang and Yan (2022) emphasized the value of examining the specific off-the-job actions CEOs take in their personal lives, such as the purchase of critical illness insurance, as determinants of CSR.

Notwithstanding these findings, the link between a CEO’s childhood experiences and CSR still remains understudied. Increasing efforts have been made in the past few years to address the enduring impact of the CEO’s difficult childhood experiences, including poverty (Xu & Ma, 2022) and famine (Han et al., 2022) on CSR. Similar to our study, O’Sullivan et al. (2021) focused on the effect of a CEO’s childhood natural disaster experience on CSR, establishing a positive relationship based on the post-traumatic growth theory. Two aspects are missing in their theoretical perspectives. First, a natural disaster is unpredictable by nature (Maki et al., 2019), and the experience of a natural disaster tends to be a collective, shared tragedy, which shifts the victim’s values to prosocial directions (Maki et al., 2019; Oishi et al., 2017). Second, the natural disaster experience can affect an individual’s risk tendency to be either risk-aversive or risk-taking (Bernile et al., 2017; Dessaint & Matray, 2017), which in turn might determine a firm’s level of CSR activities. Thus, the current study builds on O’Sullivan et al.,’s (2021) to explore both positive and negative relationships between the CEO’s childhood natural disaster experience and CSR through three different complementary mechanisms (i.e., prosocial values, risk-aversive, and risk-taking tendencies) based on the literature of psychology and finance, and further proposes CEO career horizons and community social capital as the boundary conditions.

CEO’s Childhood Disaster Experience and CSR

From the perspective of psychology, the experience of a natural disaster such as an earthquake, hurricane, or tornado can be both traumatic to individuals and disruptive to social structures. While some disasters are avoidable or may be mitigated, natural disasters happen randomly and are difficult to predict and control (Maki et al., 2019), making it hard for victims to understand why they happen (Norris et al., 2002). As a result, victims of natural disasters may turn to God to explain their experiences (Stephens et al., 2013) or search for meaning in the trauma (Maffly-Kipp et al., 2021). Furthermore, compared to traumatic experiences that tend to be specific to victims (e.g., serious illness, family difficulties, poverty, rape, and child abuse), the experience of a natural disaster is shared with other victims (Oishi et al., 2017). In this regard, the experience of a major natural disaster redirects people’s individualistic values toward collectivistic values and increases their willingness to contribute to others’ wellbeing (Oishi et al., 2017) “because ‘they’ are now ‘us’” (Drury et al., 2016, p. 210).

According to self-categorization theory, individuals tend to place themselves and others into groups based on their most salient or easily observable characteristics (Turner et al., 1987). Given the collective nature of the experience with others and the magnitude of the destructive consequences it creates (Oishi et al., 2017), individuals who experience a natural disaster are likely to identify with other victims. A growing stream of psychology literature has supported that survivors of natural disasters demonstrate prosocial behaviors toward the community, such as participating in disaster recovery efforts and making donations (Maki et al., 2019; Ntontis et al., 2018), providing each other with social support (Drury et al., 2016), and seeking prosocial occupations including firefighting (Oishi et al., 2017).

Even in a commercial setting, Dinger et al. (2020) demonstrate that the experience of natural disaster spurs local business owners in small communities to engage in post-disaster business rebuilding efforts for a highly non-economic reason, prioritizing people over money. Children who are survivors of natural disasters also display prosocial behaviors; for example, Li et al. (2013) find that the experience of an earthquake immediately increased altruistic giving among 9-year-old children. This suggests that natural disaster enhances altruism even among young children. Consistent with the premise of self-categorization theory, the individual’s tendency to help others and increase engagement in prosocial actions following the experience of natural disaster has been explained by the emergent sense of unity (Ntontis et al., 2018), common fate (Drury et al., 2016; Maki et al., 2019), and a shared social identity with others (Dinger et al., 2020; Maki et al., 2019), reflecting the shift in values from the egocentric to the allocentric direction (Oishi et al., 2017).

In summary, characterized by unexpectedness and seemingly random occurrence as well as the collective nature of the experience with others, natural disaster experienced in childhood is expected to promote individuals’ altruistic values and modes of thinking that will manifest in prosocial behaviors in adulthood. A substantial body of literature supports that CEOs’ early-life experiences influence their moral values and ethical standards throughout their lifespans (Han et al., 2022; Xu & Ma, 2022; Yao et al., 2020). According to this theoretical reasoning, it can be predicted that CEOs’ natural disaster experience in childhood will have a positive impact on their future CSR initiatives, implemented with an altruistic motive to benefit diverse stakeholders (Barnett, 2007).

The emerging literature in finance may suggest an alternative route through which the CEO’s childhood experience of natural disaster positively leads to a firm’s CSR based on how CEOs with childhood natural disaster experience become more risk-averse. Risk preferences have long been considered as a crucial personal trait of corporate managers (Kihlstrom & Laffont, 1979). Exposure to traumatic events in childhood makes individuals more sensitive to the consequences of taking risks as they focus on the downside of the risk, such as fatalities, and therefore makes them more sensitized to the consequences of risk-taking and in turn implement more risk-averse and conservative corporate policies. Therefore, firms led by CEOs who experienced trauma including a natural disaster, war, or famine in early life reduce R&D investments (Chen et al., 2022; Ru et al., 2022) and increase financial information transparency (Choi & Jung, 2021) and quality (Yao et al., 2020), because they are more cautious about decisions that increase firm risk.

Prior studies have indicated that CSR is a potential risk management tool capable of creating value for shareholders in the face of negative events because goodwill or moral capital arising from CSR can protect shareholder value (Godfrey et al., 2009). Thus, for those CEOs with risk-averse tendencies shaped by their childhood natural disaster experience, CSR will become a viable option to manage the unforeseeable future risk of the firm. From the risk-aversion perspective, consistent with the above prediction based on the psychology literature, a positive relationship between the CEO’s childhood natural disaster experience and CSR is likely. Formally,

H1a

CEOs with childhood natural disaster experience are more likely to engage in CSR.The extant literature also supports the opposite perspective that experiencing a natural disaster can make individuals less risk-averse (Gao et al., 2020) and even boost their confidence in dealing with risky situations (Zhang et al., 2022a) because “what doesn’t kill you will only make you more risk-loving” (Bernile et al., 2017, p. 167). Chen et al. (2021), for instance, reveal that firms led by CEOs with early-life natural disaster experiences are more risk-tolerant and thus more willing to accept the risks associated with bad news hoarding, resulting in higher engagement in a firm’s stock price crash risk behavior. Similarly, Bernile et al. (2017) find that CEOs who experienced early-life natural disasters tend to behave more aggressively because experiencing such disasters without extremely negative consequences desensitized them to the negative consequences of risks. When people face traumatic, life-threatening encounters, “everything else likely seems pale in comparison” (Ben-Zur & Zeidner, 2009, p. 121). In other words, to those who had near-fatal experiences, any experience that is less threatening than a life-threatening encounter will appear much less terrifying and risky (Ben-Zur & Zeidner, 2009; Taylor & Lobel, 1989).

Based on this view, given that CSR is a firm’s discretionary activity driven by altruistic motives to enhance relationships with key stakeholders (Barnett, 2007), a firm with a CEO who experienced a natural disaster in childhood may decide not to engage in CSR because of the risk-taking tendency developed by the exposure to childhood natural disasters. Therefore, with a risk-taking view, contrary to H1a, a negative relationship between CEOs with childhood natural disaster experience and CSR is proposed:

H1b

CEOs with childhood natural disaster experience are less likely to engage in CSR.

Moderating Effect of CEO Career Horizon

Although a CEO’s childhood experience of natural disaster can influence a firm’s future decision to engage in CSR, not all CEOs react in the same way. One of the key factors that influences a CEO’s strategic decision-making is their career horizon. CEO career horizon is the expected amount of time left before a CEO retires (Antia et al., 2010; Matta & Beamish, 2008). Measured by a combination of age and tenure relative to the industry average, advancing age and longer tenure shorten a CEO’s career horizon (Lee et al., 2018). CEO age (Huang et al., 2012; Serfling, 2014) and tenure (Chen et al., 2019; Finkelstein & Hambrick, 1990) have long been considered to be important demographic variables that affect the way CEOs perceive, process, and interpret information, thus influencing the corporate decisions they make.

CEOs with relatively longer career horizons have been shown to make risky decisions to prove their abilities and acquire a sound professional reputation (Prendergast & Stole, 1996) and engage more in growth and acquisitions (Matta & Beamish, 2008; Yim, 2013). By contrast, CEOs with shorter career horizons lose interest in making long-term investments such as breakthrough innovations (Cho & Kim, 2017; Lee et al., 2018; Serfling, 2014) to safeguard their reputation built over time and to avoid risking their future financial security (Davidson et al., 2007). Instead, they focus on short-term profit-generating initiatives such as sales promotion (Antia et al., 2010).

Similarly, CEOs in the later stage of their careers refrain from pursuing corporate strategies with high outcome uncertainty (Bertrand & Schoar, 2003). The CSR outcome is expected to be realized in the long run (Burke & Logsdon, 1996; Mahapatra, 1984). Therefore, when it comes to CSR, Oh et al. (2016) argued that as career horizon is shortened, CEOs are less likely to engage in CSR, because CEOs with a shorter career horizon will have a hard time envisioning the benefit from CSR activities. However, since Oh et al. (2016) did not find empirical support for the proposed positive relationship, the direct relationship between CEO career horizon and CSR is inconclusive.

This inconclusive relationship raises an important question of whether CEOs with longer career horizons will increase or decrease CSR in light of their childhood natural disaster experience. Given that CSR generates long-term pay-off (Burke & Logsdon, 1996; Mahapatra, 1984), compared to CEOs with a shorter career horizon, CEOs with a longer career horizon should be more interested in engaging in CSR, coupled with prosocial values and risk-aversive tendencies they developed as a result of experiencing natural disaster in childhood. According to this logic, CEO career horizon should moderate the positive relationship between the CEO’s childhood natural disaster experience and CSR, such that CEOs with longer career horizons are more likely to engage in CSR than CEOs with shorter career horizons when they experienced natural disaster in childhood.

H2a

CEO career horizon strengthens the positive relationship between CEO’s childhood natural disaster experience and CSR.

On the other hand, according to the well-established evidence of the variations in the corporate decisions made by CEOs with longer versus shorter horizons, CEOs with longer career horizons are more likely to engage in bolder actions because they have opportunities to rebound even if they do not go well (Prendergast & Stole, 1996). Note that CSR is a firm’s discretionary activity and may not benefit the firm directly (Barnett, 2007) and therefore it is not a must for all firms to do it. In this sense, CEO career horizon should strengthen the negative relationship between a CEO’s childhood natural disaster experience and CSR, coupled with the risk-taking tendencies developed by a CEO with childhood natural disaster experience. Therefore, a CEO with a longer career horizon and experience of childhood natural disaster is going to be less likely to engage in CSR than a CEO with a shorter career horizon and experience of childhood natural disaster.

H2b

CEO career horizon strengthens the negative relationship between a CEO’s childhood natural disaster experience and CSR.

Moderating Effect of Community Social Capital

Because each company resides within geographically bounded communities, organizations are susceptible to the social-environmental influences of the local community (Hasan et al., 2017). Although the social capital literature is extensive across various fields in the social sciences, it has not been long since an emerging body of literature has recognized the influence of the social capital of the firm’s location on various firm and managerial decisions (e.g., Hartlieb et al., 2020; Hasan et al., 2017). Following Hoi et al. (2018), we define social capital as the strength of cooperative norms and the density of social networks in local, small-scale, and geographically bounded communities. Cooperative norms are nonreligious social norms that promote individuals to share a set of common beliefs (Knack & Keefer, 1997). A dense social network facilitates effective communications and enforcement of the civic norms in the local community (Coleman, 1988). Community social capital is a by-product of social relationships stemming from social exchanges in structured social networks (Islam et al., 2006). It is a type of capital owned by the local community, thus a public good that benefits all members of the community (Putnam, 2001).

The consensus in the research on community social capital is that a high level of social capital in a local community facilitates norm-consistent behaviors and constrains norm-violating behaviors (e.g., Bowles & Gintis, 2002; Marquis & Battilana, 2009) because strong cooperative norms restrain narrow self-interest (Knack & Keefer, 1997), and dense social networks heighten social sanctions for self-serving behaviors (Coleman, 1988). In business, managers in high social capital U.S. counties exhibit less opportunistic behaviors, such as corporate tax avoidance (Hasan et al., 2017), stock price crash risk (Li et al., 2017), and asymmetric cost behaviors (Hartlieb et al., 2020), as well as committing fraud by misrepresenting financial information (Jha, 2019).

Community social capital also plays a key role in explaining a firm’s altruistic inclination to engage in CSR (Hoi et al., 2018; Jha & Cox, 2015; Marquis et al., 2007). Jha and Cox (2015) discuss how some firms might be more altruistic than others purely by virtue of where they are located, leading to higher engagement in CSR. This is explained by the high level of social capital: in regions with high social capital, managers are more ethical and altruistic while also being less self-centered (see also Hoi et al., 2018). Marquis et al. (2007) similarly argued that community social capital serves as a significant source of social-environmental pressures that give rise to CSR.

Given that a high level of social capital is a conducive condition for firms headquartered in the region to consider implementing CSR, when a positive relationship between the CEO’s childhood natural disaster experience and CSR exists due to prosocial values and/or the risk-aversive the tendencies CEO developed as a result of the experience, this relationship will be more pronounced when community social capital is high than low:

H3a

Community social capital strengthens the positive relationship between a CEO’s childhood natural disaster experience and CSR.

On the other hand, even if a negative relationship between the CEO’s childhood experience of natural disaster and CSR might exist because of the CEO’s risk-taking tendency developed by the childhood natural disaster experiences, the social-environmental pressure coming from the local community is difficult to ignore. The extant evidence favors the strong correlation between the high level of community social capital and the firm’s norm-consistent behaviors (Bowles & Gintis, 2002; Marquis & Battilana, 2009) which inform positive firm decisions. Thus, we expect that the presence of high-level community social capital will precede the CEO’s risk-taking tendency, weakening the negative relationship between a CEO’s childhood experience of natural disaster and CSR. This leads to:

H3b

Community social capital weakens the negative relationship between a CEO’s childhood natural disaster experience and CSR.

Method

Data and Sample

We collected variables from multiple secondary databases. We manually searched multiple sources such as Marquis Who’s Who, LexisNexis, Compustat, ExecuComp, and various online sources (e.g., Wikipedia, LinkedIn, and Bloomberg) for CEOs’ profiles and CEO-related covariates for S&P 1500 firms. To collect natural disaster data, we obtained the database of U.S. county-level natural disasters provided by the Federal Emergency Management Agency (FEMA). The natural disaster data incorporate disasters in each county across all 50 states between 1953 and 1990, including flood, drought, severe storm, tornado, hurricane, snow, freezing, fire, severe ice storm, coastal storm, volcano, typhoon, earthquake, and others. To identify the severe natural disaster events in the FEMA database, we only consider the natural disaster events categorized as “major disaster declarations.”

Since some CEOs were born prior to the period covered by the FEMA dataset, their exposure to natural disasters in their formative years (5–15 years) may be missing in our dataset. To construct a more comprehensive county-level natural disaster database that covered the period of all CEOs’ formative years, we searched additional data sources, which included the United States Census Bureau, the National Weather Service (NWS) of the United States National Oceanic and Atmospheric Administration (NOAA), the United States National Climate Data Center (NCDC), the International Emergency Disasters Database (EM-DAT), GenDisasters, and Wikipedia. Ultimately, we had a total of 739 unique U.S.-born CEOs of firms in the S&P 1500 in the period of 2001–2013 in our dataset.

For CSR, we used the KLD (Kinder, Lydenberg, and Domini) ratings database for the years of 2001–2013. We derived the remaining firm-related covariates and financial variables from the CRSP (Center for Research in Security Prices)-Compustat Merged database. We compiled all the variables for the baseline model and retained 3,970 firm-year observations.

Measures

CEO’s Childhood Natural Disaster Experience

Regarding CEOs’ childhood experience of natural disaster, we utilized U.S. county-level natural disaster data. By matching the number of natural disasters for each county and state with the places where the CEOs were born and spent their childhood (5–15 years; Office of Disease Prevention & Health Promotion, 2020), we created one proxy measure—the level of a CEO’s childhood natural disaster experience (CDELEV)—as an indicator that equals 1 if the CEO resided in the county where a severe natural disaster event occurred at least once between the CEO’s ages of 5 and 15 years and 0 otherwise. We only used companies for which we can identify the birthplace of the CEO in our sample. If the birthplace of a CEO was not available in any secondary database we searched, we excluded the CEO.

Overall CSR

For the CSR measure, we used KLD ratings, which have been widely used in CSR research (e.g., Meier & Schier, 2021; Servaes & Tamayo, 2013). KLD rates U.S. companies in several categories including (1) human rights, (2) environment, (3) employee relations, (4) community, (5) diversity, (6) product, and (7) corporate governance. For each dimension, strengths and concerns are scored as binary indicators. In this study, we excluded corporate governance due to its distinctive nature from the other six dimensions (Servaes & Tamayo, 2013).

We created two measures of CSR: (1) an overall CSR score and (2) an alternative measure of CSR for a robustness check for the overall CSR score. For the overall CSR score (CSR), following Benlemlih (2017), we constructed a proxy as the sum of firms’ strength scores over the six dimensions minus the sum of firms’ concern scores over the six dimensions. To check for robustness, we tested the alternative measure of CSR (SCSR) following Servaes and Tamayo’s (2013) approach and scaled the strengths and concerns for each year in the range from 0 to 1.

CEO Career Horizon

CEO career horizon has been measured simply as either CEO age or CEO tenure as a proxy (e.g., Matta & Beamish, 2008; McClelland et al., 2012; Oh et al., 2018), but this method does not consider the heterogeneity of the CEO career horizons that may exist across industries (e.g., Lucier et al., 2002). To account for such industry effect, we measured CEO career horizon (CHRZ) using the two dimensions of CEO age and tenure relative to the average CEO tenure and age from all CEOs in the same industry (Antia et al., 2010; Lee et al., 2018). This industry-adjusted measure for CEO career horizon is constructed as follows:

where \({CEO age}_{avg, t}\) is the average of all CEOs’ ages in the same four-digit SIC industry. \({CEO age}_{i,t}\) is the age of a CEO who works for firm i in year t. \({CEO tenure}_{avg, t}\) is the average number of years all CEOs have held that position in the same four digit SIC industry. \({CEO tenure}_{i,t}\) is the number of years a CEO has that position in firm i and year t. A positive (negative) CEO career horizon means that the CEO’s expected career length is longer (shorter) due to younger (older) age and/or shorter (longer) tenure than the industry average.

Community Social Capital

Following the approach adopted by Rupasingha et al. (2006), we used an aggregate social capital index (SOCA) based on data provided by the Northeast Regional Center for Rural Development (NRCRD) at Pennsylvania State University. The NRCRD data include county-level information on the following four variables: (1) percentage of eligible voters who voted in presidential elections, (2) response rate to the Census Bureau’s decennial census, (3) sum of non-profit organizations divided by populations per 10,000, and (4) sum of ten typesFootnote 1 of social organizations divided by population per 10,000, published in five different years of 1990, 1997, 2005, 2009, and 2014. This social capital index represents both the strength of cooperative norms and the density of networks (Hartlieb et al., 2020), which corresponds to the conceptualization of community social capital (Hoi et al., 2018) we adopted in this study.

The justification for using the first two variables (i.e., voter turnout and census response rate) as proxies for community social capital is that there are no legal obligations or economic incentives to vote or to take part in census surveys (Knack, 2000). Therefore, data on voter turnout and census response rate effectively capture the norms in place that govern individuals’ cooperative behaviors. The last two variables (i.e., the number of non-profit and social organizations), on the other hand, reflect the density of horizontal social networks through participation in lateral non-profit and social organizations (Coleman, 1988).

We measured social capital (SOCA) as the first principal component of a principal component analysis using the four aforementioned variables. Since the available database spans only 5 years, we completed other missing years using the available data following the previous literature (Hasan et al., 2017). For instance, we used the same social capital data published in 1990 to fill in missing data for years 1991 to 1996.

Control Variables

We utilized firm-level and CEO-related covariates. According to the slack resource theory (Waddock & Graves, 1997), firms with better financial performance have more available (i.e., slack) resources that provide them opportunities to invest in CSR. Therefore, we controlled for firm size (SIZE), firm’s return on assets (ROA), leverage (LEV), market to book ratio (MB), advertising intensity (AINT), R&D intensity (RDINT), and cash holdings (CASH), following the extant literature (e.g., Chen et al., 2019; Dadanlar & Abebe, 2020; Dupire & M’Zali, 2018; Flammer, 2015; Hasan & Habib, 2017; Hoberg & Phillips, 2010; Lee et al., 2018; Lenz et al., 2017; Luo & Bhattacharya, 2009; Meier & Schier, 2021; Servaes & Tamayo, 2013).

To take firm-level risk-taking tendency into account, we included Herfindahl Index (HHI) and firm age (FAGE; Dupire & M’Zali, 2018; Hoberg & Phillips, 2010). We also controlled for diversification of a firm’s operation including business segments (SEGMT; O’Sullivan et al., 2021). We controlled for institutional ownership (INTOWNS) and analyst coverage (ACOV), as these external monitoring mechanisms are known to affect CEOs’ discretionary spending on CSR performance (e.g., Adhikari, 2016; Chen et al., 2020).

To investigate the CEO’s risk-taking tendency as a mechanism, we adopted several proxies for CEO’s risk-taking incentives including CEO’s equity incentive (EQINC), accumulated inside debt holdings (INSDEBT), and CEO stock option (CRWTH) following the extant literature (Anderson & Core, 2018; Boubaker et al., 2020; Fabrizi et al., 2014; Martin et al., 2013). EQINC is the dollar change in the CEO’s equity portfolio for a 1% change in stock return volatility, which is deflated by CEO total cash compensation (Fabrizi et al., 2014). Fabrizi et al. (2014) showed that EQINC based on stock option captures greater CEO risk-taking tendency. INSDEBT is accumulated inside debt holdings divided by accumulated inside equity holdings, which is divided by firm debt to equity ratio (Boubaker et al., 2020). Anderson and Core (2018) and Boubaker et al. (2020) showed that accumulated inside debt holdings result in less CEO risk-taking. CRWTH is the number of options from each option grant, which is multiplied by their corresponding spread (for in the money options) on the final day of the fiscal year (Martin et al., 2013). Martin et al. (2013) showed that accumulated current wealth leads to less CEO risk-taking.

For CEO-related covariates, we controlled for CEO tenure (TENURE), CEO age (AGE), CEO duality (DUAL), CEO gender (GENDER), CEO ownership (OWNS), and insider CEO (INSIDER) because of their influences on a firm’s CSR (e.g., Chen et al., 2019; Harjoto & Laksmana, 2018; Meier & Schier, 2021; Oh et al., 2016, 2018; Yuan et al., 2019). Detailed measurements and examples of prior empirical studies that utilized the measurements of each variable are presented in Table 1.

Results

Descriptive Statistics

Table 2 presents the means, standard deviations, and correlations of the variables of interest and covariates. We confirmed that multicollinearity is not a concern in our study as all VIF scores ranged from 1.39 to 3.61, which is well below 10, as suggested by Dielman (2001).

Main Results and Analyses

We tested the fixed-effects regression model, controlling for both year and two-digit (SIC) industry fixed effects with robust standard errors adjusted for firm-level clustering. We included all the control variables defined in Table 1 in the baseline model presented in Table 3. As presented in Table 3, we analyzed the effect of CEOs’ childhood experience of natural disaster using a proxy measure (CDELEV). Model 1 includes the independent variable and the firm-level and CEO-level covariates. Models 2–4 include CEO’s equity incentive (EQINC), accumulated inside debt holdings (INSDEBT), and CEO stock option (CRWTH) in each separate model, along with the independent variables and the covariates. Lastly, Model 5 includes all the above-mentioned variables along with the independent variables and the covariates.

Across all the Models 1 through 5, we find that a CEO’s childhood experience of natural disaster has a positive influence on the focal firm’s CSR, which supports H1a and rejects H1b. For instance, in Model 1, the coefficient estimated on CDELEV (βCDELEV = 0.395, p < 0.01) implies that a firm led by a CEO with childhood experience of natural disaster tends to increase its CSR score 0.395 more than a firm led by CEO without natural disaster experience. In terms of economic significance, the coefficient estimated on the natural disaster translates into a 20% increase in relation to the interquartile range of CSR in our sample (lowest quartile: -1 and upper quartile: 1). In the later robustness analysis, we also find that the coefficient estimated on the natural disaster is associated with a 16% increase relative to the interquartile range of the scaled CSR (lowest quartile: − 0.143 and upper quartile: 0.054).Footnote 2

We further investigated the mechanism through which a firm led by a CEO with childhood natural disaster experience achieves a high CSR score. We used risk-taking tendency measures to test a potential mechanism. Table 3, Model 1 shows the baseline model without any risk-taking tendency measures. In Models 2 through 4, we interacted CDELEV with three risk-taking tendency measures (EQINC, INSIDEBT, and CRWTH), respectively. In Model 5, we included all three risk-taking tendency measures and their interactions with CDELEV.

If the prosocial values mechanism is the only significant mechanism to explain the positive relationship, risk-taking tendency measures should not affect this relationship (i.e., the interaction between CDELEV and risk-taking tendency measures will be insignificant). However, if the risk-taking or risk-aversive tendency is also a mechanism, either tendency should affect this relationship (i.e., the interaction effects will be significant). Specifically, if CEOs with childhood natural disaster experience have a greater risk-aversive tendency, the interaction between CDELEV and EQINC will be negative, while the interactions between CDELEV and INSIDEBT and between CDELEV and CRWTH will be positive. On the contrary, if CEOs with childhood natural disaster experience have a greater risk-taking tendency, the interaction between CDELEV and EQINC will be positive, while the interactions between CDELEV and INSIDEBT and between CDELEV and CRWTH will be negative.

The result in Model 2 shows a marginally significant negative interaction effect between CDELEV and EQINC (βCDELEV×EQINC = − 0.059, p < 0.10). In Models 3–5, the interactions with two risk-taking incentive measures (βCDELEV×INSIDEBT = 0.001, p < 0.05 and βCDELEV×CRWTH = 0.028, p < 0.05) consistently showed a positive and significant effect. The interaction results show that CEOs with natural disaster experience indeed respond to the suggested risk-taking or risk-aversive mechanism in that the positive effect of CDELEV on CSR is less pronounced in firms with a greater level of EQUIC, while the positive effect of CDELEV on CSR is more pronounced in firms with a greater level of INSIDEBT and CRWTH, respectively.

To provide supporting evidence, we also examined the impact of CEOs’ childhood natural disaster experience on an additional risk-taking measure of cash holdings. This supplementary analysis is presented in (See Appendix Table 7). We further observed that while the impact of disaster experience varies with the level of risk-taking tendency measures, particularly relating to being risk-averse, the coefficient estimated on CDELEV is significant at the 5% level, which might capture the positive effect of a prosocial-value mechanism.

In Table 4, to test H2a and H2b, Model 1 includes CEO career horizon (CHRZ) and the interaction term between CDELEV and CHRZ. To test H3a and H3b, Model 2 includes social capital (SOCA) and the interaction term between CDELEV and SOCA. To simultaneously test the two respective moderating effects, Model 3 includes both CHRZ and SOCA and their interaction terms, along with the independent variable (CDELEV) and the covariates. To account for region-based persistent effects, we conducted main analyses controlling for state-year fixed effects (e.g., religious ranking (RELIG) or politician orientation (POLIT) of the state in which a firm is located), as these may influence the firm’s CSR performance (Deng et al., 2013; Rubin, 2008; Zolotoy et al., 2019).

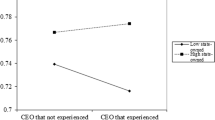

As seen in Model 1, the positive main effect is stronger when the CEO career horizon is longer (βCDELEV×CHRZ = 0.014, p < 0.05), supporting H2a and rejecting H2b. A simple slope test (Fig. 1) indicates that the positive effect of the CEO’s childhood experience of natural disaster on CSR is significant when the CEO has a longer career horizon (t = 2.01, p < 0.05), but not when the CEO has a short career horizon (t = 0.92, n.s.).

Moderating effects of CEO career horizons

Model 2 shows that the positive effect of a CEO’s childhood experience of natural disaster on CSR is stronger when the firm is located in a community with a higher level of community social capital (βCDELEV×SOCA = 0.218, p < 0.05), which supports H3a and rejects H3b. A simple slope test confirms that the positive effect of the CEO’s childhood experience of natural disaster on CSR is significant when the community has a high level of social capital (t = 2.27, p < 0.05), but not when the community has a low level of social capital (t = 1.05, n.s.).

Furthermore, as shown in Model 3, when considering both moderators together, the moderating effects of CEO career horizon and social capital are both positive (βCDELEV×CHRZ = 0.012, p < 0.05; βCDELEV×SOCA = 0.191, p < 0.05). Taken together, the results indicate that the positive relationship between CDELEV and CSR is enhanced as the CEO career horizon is longer and the level of community social capital is higher (Fig. 2).

Moderating effects of social capital

Table 5 presents post-hoc analyses to examine each of the six dimensions of CSR separately to understand their relationships with the CEO’s childhood experience of natural disaster. As seen in Table 5, CDELEV had significantly positive effects on the environment, employee relations, community, diversity, and product CSR dimensions. CDELEV did not show a significant influence on the human rights CSR dimension.

Robustness Tests

A conclusive endogeneity correction cannot be made in this research setting. Specifically, controlling for potential self-selection of managers with childhood disaster experience is challenging, given that natural disasters themselves are regarded as exogenous nature-driven events. Our study benefits from adopting the variable of the CEO’s childhood experience of natural disaster from the archival data as opposed to an individual’s self-reported traumatic event experience which may result in reporting bias (Bernile et al., 2017; Chen et al., 2021). However, we conducted the following analyses to alleviate concerns about possible endogeneity issues.

To provide more rigorous causal inferences, all the independent variables, moderators, and covariates across all the models were lagged by one year (e.g., Oh & Barker, 2018). To account for aggregate industry conditions and time trends, we included industry-year fixed effects in the models that used robust standard errors adjusted for firm-level clustering. In addition, to address any measurement concerns and ensure the robustness of our main results, we conducted a similar analysis using an alternative dependent variable, scaled CSR (SCSR), measured as the CSR strengths and concerns scaled by the maximum strengths and concerns any firm has in the fiscal year (Servaes & Tamayo, 2013). As presented in Panel A of Table 6, the result of the main analysis using SCSR as a dependent variable showed the positive effect of a CEO’s childhood experience of natural disaster on CSR (βCDELEV = 0.031, p < 0.01).

As reported in Panel B, we re-estimated the baseline model by using the sample of CEOs who were born in low-migration states. There might be a potential concern that an individual moved to another location with their family during their early formative years. While we acknowledge that we could not completely track our sample CEOs’ location changes in their childhood, we conducted a subsample analysis. We rely on the assumption that CEOs and their families were less likely to change their locations in a state featuring a low level of migration recorded during their early childhood. Low-migration states are identified if the number of out-migrants during the CEO’s childhood period (ages of 5 and 15 years) scaled by the state population for the period is less than the average number of out-migrants scaled in the United States for the same period according to the United States Census Bureau. The result confirms the persistent positive effect of a CEO’s childhood experience of natural disaster on CSR (βCDELEV = 0.989, p < 0.05) (Table 7).

We also included CEO birth state and birth year to control for firm fixed-effects in the models presented in Panel C. Inclusion of firm fixed effects absorbs time-invariant firm attributes. Inclusion of CEO birth state fixed effects absorbs time-invariant factors at the state level. Inclusion of CEO birth year fixed effects controls for possible cohort-related effects (Bernile et al., 2017; Chen et al., 2021). After accounting for the firm fixed effect along with multiple covariates, we found a positive effect of CEO’s childhood experience of natural disaster on CSR (βCDELEV = 0.246, p < 0.05).

We re-estimated our baseline model using the matched sample based on the Propensity Score Matching (PSM) technique. It is possible that some unknown factors influence both the decision of a CEO with childhood natural disaster experience to join a firm and the firm’s CSR policies. To mitigate this endogeneity concern, we closely followed the matching procedure of PSM sample construction suggested by Chen et al. (2021). The results are presented in Panel D. We found a positive effect of CEO’s childhood experience of natural disaster on CSR (βCDELEV = 0.364, p < 0.01).

As a final robustness check, we tested the causal effect of CEO’s childhood experience of natural disaster on CSR by examining the changes in CSR around CEO turnover events. Following the literature (Chen et al., 2021), we obtained information on CEO turnover events from the ExecuComp database. We maintained turnover events only if there is a change in CEO’s childhood natural disaster experiences. In other word, if the former CEO has childhood disaster experience and the incoming CEO does not, or if the former CEO does not have childhood disaster experience and the incoming CEO does, those turnover events are retained. For each CEO turnover event occurring in year t (e.g., 2003), the change in CSR score is calculated by subtracting the average CSR scores in the two years pre-CEO turnover (t-2, t-1, e.g., average CSR score between 2001 and 2002] from the average CSR scores in the two years post-CEO turnover (t + 1, t + 2; e.g., average CSR score between 2004 and 2005].

As presented in Panel E, there were a total of 103 turnover events, with 45 turnovers from CEO without disaster experience to CEO with disaster experience and 58 turnovers from CEO with disaster experience to CEO without disaster experience. The result showed that CSR increased when the turnover occurred from CEO without disaster experience to CEO with disaster experience (βCDELEV = 0.109, p < 0.05) and decreased when the turnover occurred from CEO with disaster experience to CEO without disaster experience (βCDELEV =—0.181, p < 0.10). The difference between the two cases was significant (βCDELEV = 0.290, t = 2.1, p < 0.05), indicating the positive causal effect of CEO childhood natural disaster experience on CSR.

Discussion

Theoretical, Managerial, Ethical Implications

A wide range of personal experiences, especially traumatic events in childhood and adverse early-life experiences, can have a profound impact on people’s perceptions and behaviors. CEOs’ early-life experiences influence their moral values and ethical standards throughout their lifespans (Han et al., 2022; Xu & Ma, 2022; Yao et al., 2020). This study aimed to explore the relationship between a CEO’s childhood experience of natural disasters and their ethical behavior, specifically engaging in CSR. Using a sample of U.S. firms for the 2001–2013 period, the findings reveal that companies led by CEOs with experience of a natural disaster in childhood show higher levels of CSR performance. In addition, we find that this tendency is stronger when the CEO has a longer career horizon and if the community social capital is high. These findings have several implications.

First, this study extends the existing line of research focusing on how a CEO’s personal preferences driven by their unique experiences, values, and personality traits affect their firm’s CSR policies based on the upper echelons theory (e.g., Boone et al., 2020; Liu et al., 2017; Petrenko et al., 2016; Sajko et al., 2021). Recent upper echelons theory proponents have highlighted that not only has limited research been dedicated to within-firm determinants as opposed to externally driven determinants of CSR (Al-Shammari et al., 2019; Chin et al., 2013), but very few researchers have recognized that the level of CSR activities might be dependent, at least in part, on the CEO’s characteristics or priorities (Al-Shammari et al., 2019). Different from prior studies that examined a CEO’s professional career experiences such as tenure (Chen et al., 2019; Finkelstein & Hambrick, 1990), military (Nasih et al., 2019; Zhang et al., 2022b) or overseas work experiences (Slater & Dixon-Fowler, 2009) in adulthood, we focused on the CEOs’ off-the-job (Wang & Yan, 2022) and non-work-related (Tian et al., 2022) early childhood experience in connection with CSR. Our empirical results clearly reveal that a CEO’s childhood experience of natural disaster makes a significant difference in whether their firm engages in CSR and that this is a useful yet under-explored variable that can help explain the substantial variations in firms’ CSR performance.

Second, the findings of this study add new evidence to the literature on the impact of a CEO’s childhood experience of natural disaster on corporate decision-making. As Tian et al., (2022, p. 1) put it, “the impact of childhood trauma exposure on CEOs’ strategic decision-making is not well understood”. Although the role of the CEO is crucial in predicting a firm’s commitment to CSR (Chen et al., 2019; Orlitzky et al., 2017; Yuan et al., 2019), prior researchers predominantly focused on corporate-level financial decisions (Bernile et al., 2017; Chen et al., 2021; Dessaint & Matray, 2017; Yao et al., 2020) or individual manager-level risk tendency (Bernile et al., 2021; Bui et al., 2019; De Blasio et al., 2018) as the outcomes of a CEO’s early-life disaster experience. Therefore, this study extends the resultant outcomes of such experience to CSR and contributes to this line of literature by illuminating CEO’s childhood natural disaster experience as an antecedent of a firm’s engagement in CSR.

Third, to better understand the relationship between the CEO’s childhood experience of natural disaster and CSR, we relied on the psychology and finance literature and proposed competing hypotheses using three theories that go beyond O’Sullivan et al.’s (2021) use of the post-traumatic growth theory, since the impact of childhood experience of natural disaster is too complex to be explained by a single mechanism. Acknowledging that natural disaster experiences can affect a shift in values to a prosocial direction based on the psychology literature and in risk preferences (both risk-aversion and risk-taking) based on the finance literature, we more comprehensively examined this phenomenon. Through this empirical examination, we reiterated the positive relationship consistent with the findings of O’Sullivan et al. (2021) while concluding that this relationship is jointly explained by the prosocial and the risk-aversion mechanisms. Accordingly, we further open the “black box” regarding the relationship between a CEO’s childhood experience of natural disaster and the ethical firm behavior of CSR.

Fourth, investigations of the influences of the natural disaster experience have largely centered on adults as research subjects in both the business (Bernile et al., 2021; Bui et al., 2019; De Blasio et al., 2018; Dessaint & Matray, 2017; Dinger et al., 2020) and non-business domains (Drury et al., 2016; Maki et al., 2019; Ntontis et al., 2018; Oishi et al., 2017). However, an investigation of the long-lasting effect of the childhood experience of natural disaster on prosocial behaviors toward the community including CSR has been largely missing (Masten & Narayan, 2012; Masten & Osofsky, 2010; Peek et al., 2018). Moreover, much of the extant literature on the enduring impact of CEOs’ adverse childhood experiences on firm decisions has narrowly focused on personal disasters such as poverty (Drennan et al., 2005; Xu & Ma, 2022) or other hardships including parental loss or divorce and family move (Drennan et al., 2005; Henderson & Hutton, 2018) rather than natural disaster. To this end, we draw on insights from imprinting theory to suggest that CEOs develop persistent imprints based on their childhood experience of natural disaster which last long enough to influence their future firm-level strategic decisions.

Fifth, by identifying CEO career horizon and community social capital as two important variables that moderate the positive relationship between a CEO’s childhood experience of natural disasters and CSR, we enrich the understanding of why strategic decisions made by CEOs vary despite similar childhood natural disaster experience. Even if most extant imprinting studies tend to suggest that an imprint has a uniform effect (Marquis & Tilcsik, 2013), our findings suggest that the CEO’s individual characteristics and the community-level characteristics are also important considerations to understand the phenomenon of imprinting more precisely. A previous attempt to establish a positive relationship between the CEO career horizon and CSR failed (Oh et al., 2016). There could be three reasons for this. First, Oh et al. (2016) only used age as a proxy for CEO career horizon and controlled tenure for the examination. Second, they did not take industry variance into consideration. Third, they only examined the monotonic influence of CEO career horizon, rather than in combination with other contextual variables. Thus, by highlighting how CEOs with a longer career horizon are more likely to engage in CSR when they have the childhood experience of natural disaster, our study emphasizes that the CEO’s age alone does not sufficiently reflect the CEO career horizon and to more precisely predict a firm’s CSR, the contextual influence of the CEO’s experience should not be ignored.

When it comes to community social capital, our study supplements the existing line of research focusing on how high community social capital becomes a fertile ground for a firm’s engagement in CSR (Hoi et al., 2018; Jha & Cox, 2015; Marquis et al., 2007). Consistently, our findings strongly support that when the firm’s headquarters is geographically located in an area with the high level of community social capital, it is more likely to conduct CSR when a CEO experienced natural disaster in childhood. Firms are dynamic in nature and no firms exist separate from society. Firms grow in the support of the community members particularly in the presence of strong cooperative norms and dense social networks (Hoi et al., 2018) and they in turn influence a firm’s altruistic inclination by serving as a significant source of social-environmental pressure (Marquis et al., 2007). Thus, being located in an area with a high level of social capital is a strong indicator that a firm with a CEO who experienced natural disaster in childhood is likely to conduct CSR.

For practitioners, this study emphasizes the importance of considering the CEO’s distinctive individual characteristics, namely childhood experiences and career horizons, as well as community characteristics as factors that affect a firm’s CSR performance. Consistent with previous findings that CEOs’ early-life experiences influence their ethical standards throughout their lifespans (Han et al., 2022; Xu & Ma, 2022; Yao et al., 2020), we find that CEOs’ childhood experience of natural disaster is a positive precursor to a firm’s involvement in CSR. This is good news since there is rising evidence of various factors relating to CEOs’ personal experiences that contribute to ethical lapses, which consequently lead to diminishing firm valuation (e.g., Miller & Xu, 2019). However, from an ethical point of view, this does not mean that childhood adversity is necessary, or that one way to enhance a firm’s CSR is to seek out those who experienced natural disasters in their early life. Instead, our findings support that CEOs who experienced natural disaster in childhood develop stronger prosocial values and risk-aversive tendencies compared to others, which translates into engagement in CSR. Therefore, offering organizational support for CEOs who experienced childhood adversity to carry out CSR activities will help them cope with potentially traumatic experiences for the sake of their own mental health and wellbeing and benefit the larger group of stakeholders including societies and local communities.

In addition, firms headed by CEOs with a longer career horizon in addition to natural disaster experience in childhood are more inclined to participate in CSR activities. In addition, firms headed by CEOs with natural disaster experience in childhood are more likely to conduct CSR when their headquarters are located in a community with a high level of cooperative norms and a dense social network. These findings have practical implications that firms should not simply assume a direct influence of the CEO’s childhood experience of natural disaster on CSR but should consider other individual characteristics of the CEO as well as the contextual characteristics of the community when predicting the CEO’s commitment to CSR performance.

Limitations and Future Research

Despite the theoretical and managerial contributions outlined above, our study is not without limitations. First, our study was conducted based on U.S. firms, and therefore our findings may not be generalizable to other countries with different cultures and environments. Future researchers could examine how different cultural characteristics (e.g., collectivism vs. individualism; Hofstede, 1984) may interact with the main effect of a CEO’s childhood experience of natural disaster on CSR. In addition, the scope of our research was based on S&P 1500 firms to allow a reasonable sample size and to access readily available public databases. However, future researchers are advised to expand their scope of investigation to firms with different characteristics such as B-Lab certified companies with a high level of CSR involvement or family businesses to further enhance the theoretical contribution.

Second, we did not directly measure all three proposed underlying mechanisms behind the CEO’s childhood experience of natural disaster/CSR relationship, since a measurement of the CEO’s psychological assessment that matches with the public archival data was not available. Future researchers should conduct interviews or surveys with CEOs to clearly understand the processes that explain why those who experienced natural disasters in their childhood are likely to engage in CSR.

Third, while natural disasters are characterized by a collective tragedy shared with other victims (Oishi et al., 2017), personal tragedy experiences specific to individual victims, such as serious illness, family difficulties, rape, and child abuse, may have different influences on corporate-level CSR decisions. Although researchers have started to explore the impact of personal disaster in a CEO’s childhood (e.g., childhood trauma caused by a loss of a parent, family move, and other types of hardship) and its influence on firms’ financial decisions (Henderson & Hutton, 2018), future researchers may wish to evaluate whether the CEO’s childhood experience of natural disaster and CSR relationship explored in this study is similar to the effects of a CEO’s personal disaster.

Fourth, recent studies have extensively noted a wide variety of CEO personality traits and how they affect CSR, such as overconfidence (McCarthy et al., 2017), narcissism (Al-Shammari et al., 2019; Petrenko et al., 2016; Tang et al., 2018), materialism (Davidson et al., 2019), and hubris (Tang et al., 2018). We identified the CEO’s career horizon, an additional CEO-specific characteristic, as a moderating variable, but studying the interaction effect between the various other CEO personality traits and the CEO’s childhood experience of natural disaster on CSR will present ample opportunities for future work. Moreover, there are many other individual difference variables that might interact with childhood natural disaster experience. For instance, given that adaptation to climate change is an emerging research topic in the literature (e.g., Ng et al., 2018), future researchers might wish to explore if adaptation to the natural disaster varies across CEOs and if that moderates the effect of the CEO’s natural disaster experience on their CSR.

Lastly, the current literature offers mixed views on CSR in relation to valuation. One view is that CSR leads to positive effects on valuation since strong CSR policies are well aligned with the interest of stakeholders (Lins et al., 2017). A competing view is that CSR activities are potentially detrimental to the firm valuation because CSR policies are driven by agency issues to extract private rents from stakeholders. In this view, CSR investments are negative NPV (net present value) projects for stakeholders (Krüger, 2015; Masulis & Reza, 2015). Given these mixed views, future researchers should examine how a CEO’s childhood experience of natural disaster influences the optimal level of CSR from a firm value perspective.

Data availability

All data are publicly available from sources identified in the text.

Notes

The ten types of social organizations include religious organizations, civic and social associations, business associations, political organizations, professional organizations, labor organizations, bowling centers, physical fitness facilities, public golf courses, and number of sports clubs, managers, and promoters.

Because the measure of CSR encompasses both strengths and concerns, which may cancel out each other when calculating the mean, we considered the effect of a CEO with childhood natural disaster experience on the interquartile spread of CSR instead of the sample mean. We appreciate this suggestion made by an anonymous reviewer.

References

Adhikari, B. K. (2016). Causal effect of analyst following on corporate social responsibility. Journal of Corporate Finance, 41, 201–216.

Adhikari, B. K. (2018). Female executives and corporate cash holdings. Applied Economics Letters, 25(13), 958–963.

Al-Shammari, M., Rasheed, A., & Al-Shammari, H. A. (2019). CEO narcissism and corporate social responsibility: Does CEO narcissism affect CSR focus? Journal of Business Research, 104, 106–117.

Anderson, J. D., & Core, J. E. (2018). Managerial incentives to increase risk provided by debt, stock, and options. Management Science, 64(9), 4408–4432.

Antia, M., Pantzalis, C., & Park, J. C. (2010). CEO decision horizon and firm performance: An empirical investigation. Journal of Corporate Finance, 16(3), 288–301.

Balasubramaniam, V. (2021). Lifespan expectations and financial decisions: Evidence from mass shootings and natural disaster experiences. SSRN Journal. https://doi.org/10.2139/ssrn.3289627

Barnett, M. L. (2007). Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Academy of Management Review, 32(3), 794–816.

Benlemlih, M. (2017). Corporate social responsibility and firm debt maturity. Journal of Business Ethics, 144(3), 491–517.

Ben-Zur, H., & Zeidner, M. (2009). Threat to life and risk-taking behaviors: A review of empirical findings and explanatory models. Personality and Social Psychology Review, 13(2), 109–128.

Bernile, G., Bhagwat, V., & Rau, P. R. (2017). What doesn’t kill you will only make you more risk-loving: Early-life disasters and CEO behavior. Journal of Finance, 72(1), 167–206.

Bernile, G., Bhagwat, V., Kecskés, A., & Nguyen, P. A. (2021). Are the risk attitudes of professional investors affected by personal catastrophic experiences? Financial Management, 50(2), 455–486.

Bertrand, M., & Schoar, A. (2003). Managing with style: The effect of managers on firm policies. The Quarterly Journal of Economics, 118(4), 1169–1208.

De Blasio, G., De Paola, M., Poy, S., & Scoppa, V. (2018). Risk aversion and entrepreneurship: New evidence exploiting exposure to massive earthquakes in Italy. IZA (Institute of Labor Economics) Discussion Papers, 12057. https://www.econstor.eu/bitstream/10419/193351/1/dp12057.pdf

Boone, C., Buyl, T., Declerck, C. H., & Sajko, M. (2020). A neuroscience-based model of why and when CEO social values affect investments in corporate social responsibility. The Leadership Quarterly, 33(3), 101386.

Boubaker, S., Chebbi, K., & Grira, J. (2020). Top management inside debt and corporate social responsibility? Evidence from the US. The Quarterly Review of Economics and Finance, 78, 98–115.

Bowles, S., & Gintis, H. (2002). Social capital and community governance. The Economic Journal, 112(483), F419–F436.

Bui, D. G., Hasan, I., Lin, C. Y., & Zhang, G. (2019). Natural-disaster experience and risk-taking behaviors: Evidence from individual investor trading. SSRN Journal. https://doi.org/10.2139/ssrn.3416008

Burke, L., & Logsdon, J. M. (1996). How corporate social responsibility pays off. Long Range Planning, 29(4), 495–502.

Chen, C., He, Y., Wang, K., & Yan, S. (2022). The impact of early-life natural disaster experiences on the corporate innovation by CEOs. Emerging Markets Finance and Trade., 58(14), 3953–3975.

Chen, T., Dong, H., & Lin, C. (2020). Institutional shareholders and corporate social responsibility. Journal of Financial Economics, 135(2), 483–504.

Chen, W. T., Zhou, G. S., & Zhu, X. K. (2019). CEO tenure and corporate social responsibility performance. Journal of Business Research, 95, 292–302.

Chen, Y., Fan, Q., Yang, X., & Zolotoy, L. (2021). CEO early-life disaster experience and stock price crash risk. Journal of Corporate Finance, 68, 101928.

Chin, M. K., Hambrick, D. C., & Treviño, L. K. (2013). Political ideologies of CEOs: The influence of executives’ values on corporate social responsibility. Administrative Science Quarterly, 58, 197–232.

Cho, S. Y., & Kim, S. K. (2017). Horizon problem and firm innovation: The influence of CEO career horizon, exploitation and exploration on breakthrough innovations. Research Policy, 46(10), 1801–1809.

Choi, S., & Jung, H. (2021). Does early-life war exposure of a CEO enhance corporate information transparency? Journal of Business Research, 136, 198–208.

Coleman, J. S. (1988). Social capital in the creation of human capital. American Journal of Sociology, 94, S95–S120.

Cox, C. J., & Cooper, C. L. (1989). The making of the British CEO: Childhood, work experience, personality, and management style. Academy of Management Perspectives, 3(3), 241–245.

Dadanlar, H. H., & Abebe, M. A. (2020). Female CEO leadership and the likelihood of corporate diversity misconduct: Evidence from S&P 500 firms. Journal of Business Research, 118, 398–405.

Davidson, R. H., Dey, A., & Smith, A. J. (2019). CEO materialism and corporate social responsibility. The Accounting Review, 94(1), 101–126.

Davidson, W. N., Xie, B., Xu, W., & Ning, Y. (2007). The influence of executive age, career horizon and incentives on pre-turnover earnings management. Journal of Management & Governance, 11(1), 45–60.

Deng, X., Kang, J. K., & Low, B. S. (2013). Corporate social responsibility and stakeholder value maximization: Evidence from mergers. Journal of Financial Economics, 110(1), 87–109.

Deshmukh, S., Goel, A. M., & Howe, K. M. (2021). Do CEO beliefs affect corporate cash holdings? Journal of Corporate Finance, 67, 101886.

Dessaint, O., & Matray, A. (2017). Do managers overreact to salient risks? Evidence from hurricane strikes. Journal of Financial Economics, 126(1), 97–121.

Dielman, T. E. (2001). Applied regression analysis for business and economics. Duxbury/Thomson Learning, Pacific Grove, CA.