Abstract

We examine the equity valuation effect of press releases of upgrades or downgrades reflected in the Covalence Ethical Quote (CEQ), an index ranking the ethical performance of multinational firms. The index is updated quarterly and is comprehensive enough to include 45 criteria reflecting working conditions, impact of product, impact of production, and company institutional impact. Thus, it captures many dimensions of firms’ ethical performance that are not accounted for in previous research. Our research encompasses a joint test of the value relevance of the index itself and the impact of ethical reputation on a firm’s value. We find first a significant causal relationship between stock market reactions and changes in the CEQ. Specifically, disclosures of positive (negative) changes in firm ethical performance cause increases (decreases) in firm value. Second, cross-sectional analysis indicates a positive association between changes in firm ethical performance and both its financial performance and its financial reporting quality. Collectively, these results suggest that the CEQ conveys information that is useful to investors. Further, corporate measures taken to increase ethical performance are associated with positive benefits to shareholders. Finally, investors have concluded that good news about their firms’ efforts to be ethical is worth the cost.

Similar content being viewed by others

Notes

AT&T Tops Covalence Ethical Ranking of U.S. Telecoms; Dallas, Texas, Pewaukee, Wisconsin, February 18, 2010. Source: News release.

L'Oreal Recognized As One of The World’s Most Ethical Companies; NEW YORK, March 20, 2014. Source: PR Newswire.

The 12 Least Ethical Companies In The World: Covalence's Ranking (PHOTOS, POLL) Huffington Post, Grace Kiser. First Posted: 03/30/10 06:12 AM ET; Updated: 05/25/11 04:20 PM ET.

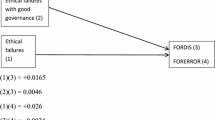

The finding of a significant association between the CEQ rankings and share prices would suggest both that the index reflects valuable information about corporate ethics and that this information is important to investors. A finding of no significance could result if either the CEQ is not a good proxy for ethical reputation and/or if shareholder wealth is not impacted by corporate ethics.

One such example is the “Business Ethics Best Citizen” title awarded by Business Week in 2001.

The authors recognize that no single, currently available measure of ethical performance is unquestioned as to what is being captured. In the conclusion section, we address some concerns regarding the CEQ specifically.

For the time period covered by this study, CEQ was based on 45 criteria. By July 2013, this had been expanded to 50 criteria.

By July 2013, the number of firms covered by the CEQ had been increased to 2,800.

We also tried to retain four factors. The eigenvalues, loadings, and variances extracted are similar both before and after rotations using Varimax or Promax.

The number of announcements cited here does not include the 114 quarterly affirmations, i.e., no change in ethical performance.

The authors are deeply indebted to the Editor for his contributions to the ideas expressed in the following three paragraphs.

References

Bakan, J. (2004). The corporation—The pathological pursuit of profit and power. New York: Simon & Schuster.

Ballou, B., Godwin, N., & Shortridge, R. (2003). Firm value and employee attitudes on workplace quality. Accounting Horizons, 17, 329–341.

Banerjee, S. B. (2008). Corporate social responsibility: The good, the bad and the ugly. Critical Sociology, 34(1), 51–79.

Barnett, M. L., & Solomon, R. M. (2006). Beyond dichotomy: The curvilinear relationship between social responsibility and FP. Strategic Management Review, 27, 1101–1122.

Baron, D., Harjoto, M., & Jo, H. (2011). The economics and politics of corporate social performance. Business and Politics, 13(2), 1–46.

Beavers, A. S., Lounsbury, J. W., Richards, J. K., Huck, S. W., Skolits, G. J., & Esquivel, S. L. (2013). Practical considerations for using exploratory factor analysis in educational research. Practical Assessment, Research & Evaluation, 18(6), 1–13.

Black, F. (1986). Noise. Journal of Finance, 41, 529–543.

Chatterji, A. K., Levine, D. I., & Toffel, M. W. (2009). How well do social ratings actually measure corporate social responsibility? Journal of Economics & Management Strategy, 18(1), 125–169.

Chatterji, A. K., & Toffel, M. W. (2010). How firms respond to being rated. Strategic Management Journal, 31, 917–945.

Chih, H. L., Shen, C. H., & Kang, F. C. (2008). Corporate social responsibility, investor protection, and earnings management: Some international evidence. Journal of Business Ethics, 79, 179–198.

Choi, T. H., & Pae, J. (2011). Business ethics and FRQ: Evidence from Korea. Journal of Business Ethics, 103, 403–427.

Clarkson, P., Li, Y., & Richardson, G. (2004). The market valuation of environmental capital expenditures by pulp and paper companies. The Accounting Review, 79(2), 329–353.

Cohen, J. R., Krishnamoorthy, G., & Wright, A. (2004). The corporate governance mosaic and financial reporting quality. Journal of Accounting Literature, 23, 87–152.

Corrado, C. J. (1989). A nonparametric test for abnormal security-price performance in event studies. Journal of Financial Economics, 23(2), 385–396.

Costello, A. B., & Osborne, J. W. (2005). Best practices in exploratory factor analysis: Four recommendations for getting the most from your analysis. Practical Assessment. Research & Evaluation, 10, 1–9.

Dechow, P. M., & Dichev, I. (2002). The quality of accruals and earnings: The role of accrual estimation errors. The Accounting Review, 77(Supplement), 35–59.

Delmas, M. A., Etzion, D., & Nairn-Birch, N. (2013). Triangulating environmental performance: What do corporate social responsibility ratings really capture? The Academy of Management Perspectives, 27(3), 255–267.

Doh, J. P., Howton, S. D., Howton, S. W., & Siegel, D. S. (2010). Does the market respond to an endorsement of social responsibility? The role of institutions, information, and legitimacy. Journal of Management, 36(6), 1461–1485.

Dyllick, T., & Hockerts, K. (2002). Beyond the business case for corporate sustainability. Business Strategy and the Environment, 11(2), 130–141.

Entine, J. (2003). The myth of social investing: A critique of its practice and consequences for corporate social performance research. Organization & Environment, 20(10), 1–17.

Fabrigar, L. R., Wegener, D. T., MacCallum, R. C., & Strahan, E. J. (1999). Evaluating the use of exploratory factor analysis in psychological research. Psychological Methods, 4, 272–299.

Fama, E. F., & French, K. R. (1993). Common risk factor in the returns on stock and bonds. Journal of Financial Economics, 33(1), 3–56.

Fama, E. F., & French, K. R. (1997). Industry costs of equity. Journal of Financial Economics, 43, 153–197.

Feldman, S. J., Soyka, P. A., & Ameer, P. G. (1997). Does improving a firm’s environmental management system and environmental performance result in a higher stock price? The Journal of Investing, 6(4), 87–97.

Field, A., Miles, J., & Field, Z. (2012). Discovering Statistics Using R. Thousand Oaks, CA: Sage.

Fischer, K., & Khoury, N. (2009). The impact of ethical rating on Canadian security performance: Portfolio management and corporate governance implications. http://www.ssrn.com.

Francis, B., Hasan, I., Park, J. C., & Wu, Q. (2009). Gender differences in financial reporting decision-making: Evidence from accounting conservatism. SSRN 1471059. www.papers.ssrn.com.

Geczy, C., Stambaugh, R. F., & Levin, D. (2005). Investing in socially responsible mutual funds. Working Paper. SSRN. http://ssrn.com/abstract=416380.

Giacotto, C., & Sfiridis, J. M. (1996). Hypothesis testing in event studies: The case of variance changes. Journal of Economics and Business, 48(4), 349–370.

Gond, J.-P., & Crane, A. (2010). Corporate social performance disoriented: Saving the lost paradigm. Business & Strategy, 49(4), 677–703.

Gray, R. (2000). Current developments and trends in social and environmental auditing, reporting and attestation: A review and comment. International Journal of Auditing, 4, 247–268.

Gray, R. (2006). Social, environmental and sustainability reporting and organisational value creation? Whose value? Whose creation? Accounting, Auditing & Accountability Journal, 19(6), 793–819.

Griffin, J., & Mahon, J. (1997). The corporate social performance and corporate financial performance debate: Twenty-five years of incomparable research. Business and Society, 36(1), 5–31.

Guerard, J. B., Jr. (1997). Is there a cost to being socially responsible in investing? Journal of Forecasting, 16(7), 475–490.

Gul, F. A., Srinidhi, B., & Tsui, J. (2011). Female directors and earnings quality. Contemporary Accounting Research, 28(5), 1610–1644.

Gunthorpe, D. L. (1997). Business ethics: A quantitative analysis of the impact of unethical behavior on publicly traded corporations. Journal of Business Ethics, 16, 537–543.

Haigh, M. (2006). Camouflage play: Making moral claims in managed investments. Accounting Forum, 30(3), 267–283.

Hawken, P. (2004). Socially responsible investing: How the SRI industry has failed to respond to people who want to invest with conscience and what can be done to change it. Sausalito: Natural Capital Institute.

Hong, Y., & Anderson, M. L. (2011). The relationship between corporate social responsibility and earnings management: An exploratory study. Journal of Business Ethics, 104(4), 461–471.

Ittner, C., & Larcker, D. (1998). Are non-financial measures leading indicators of financial performance? An analysis of customer satisfaction. Journal of Accounting Research, 36, 1–35.

Jo, H., & Harjoto, M. A. (2011). Corporate governance and firm value: The impact of corporate social responsibility. Journal of Business Ethics, 103, 351–383.

Jo, H., & Harjoto, M. A. (2012). The causal effect of corporate governance on corporate social responsibility. Journal of Business Ethics, 106(1), 53–72.

Jones, J. (1991). Earnings management during import relief investigations. Journal of Accounting Research., 29, 193–228.

Kahn, R. N., Lekander, C., & Leimkuhler, T. (1997). Just say no? The investment implications of tobacco divestiture. The Journal of Investing, 6(4), 62–70.

Kieso, D., Weygandt, J., Warfield, T., Young, N., Wiecek, I., & McConomy, B. (2013). Intermediate accounting (10th Canadian ed.). Toronto: Wiley.

Kim, Y., Park, M. S., & Wier, B. (2012). Is earnings quality associated with corporate social responsibility? The Accounting Review, 87(3), 761–796.

Klassen, R. D., & McLaughlin, C. P. (1996). The impact of environmental management of firm performance. Management Science, 42, 1199–1214.

Kothari, S. P., Leone, A., & Wasley, C. (2005). Performance matched discretionary accrual measures. Journal of Accounting and Economics, 39, 163–197.

Krishnan, G. P., & Parsons, L. M. (2008). Getting to the bottom line: An exploration of gender and earnings quality. Journal of Business Ethics, 78(1–2), 65–76.

Labelle, R., Gargouri, R. M., & Francoeur, C. (2010). This diversity management, and FRQ. Journal of Business Ethics, 93, 335–353.

Lyon, J., & Maher, M. (2004, April). The importance of business risk in setting audit fees: Evidence from cases of client misconduct. Working Paper.

Margolis, J. D., Elfenbein, H. A., & Walsh, J. P. (2007). Does it pay to be good? A meta-analysis and redirection of research on the relationship between corporate social and FP. Working Paper, Ann Arbor. www.stakeholder.bu.edu.

Margolis, J. D., & Walsh, J. P. (2003). Misery loves companies: Rethinking social initiatives by businesses. Administrative Science Quarterly, 48, 268–305.

McGuire, J. B., Sundgren, A., & Schneeweis, T. (1988). Corporate social responsibility and firm financial performance. Academy of Management Journal, 31, 854–872.

Milne, M. J. (1996). On sustainability, the environment and management accounting. Management Accounting Research, 7(1), 135–161.

Milne, M. J. (2013). Phantasmagoria, sustain-a-babbling in social and environmental reporting. In J. L. Davison & R. Craig (Eds.), The Routledge companion to accounting communication (Chap. 9, pp. 135–153). London: Routledge.

Milne, M. J., & Gray, R. (2013). W(h)ither ecology? The triple bottom line, the global reporting initiative, and corporate sustainability reporting. Journal of Business Ethics, 118(1), 13–29.

Orlitzky, M. (2013). Corporate social responsibility, noise, and stock market volatility. The Academy of Management Perspectives, 27(3), 238–254.

Orlitzky, M., Schmidt, F. L., & Rynes, S. L. (2003). Corporate social and FP: A meta-analysis. Organization Studies, 24(1), 403–441.

Peloza, J. (2009). The challenge of measuring financial impacts from investments in corporate social performance. Journal of Management, 35(6), 1518–1541.

Pett, M., Lackey, N., & Sullivan, J. (2003). Making sense of factor analysis. Thousand Oaks, CA: Sage.

Poynder, J. (1844). Literary extracts (Vol. 1). London: J. Hatchard.

Roman, R., Hayibor, S., & Agle, B. (1999). The relationship between social and FP-repainting a portrait. Business and Society, 39(1), 109–125.

Salewski, M., & Zülch, H. (2012). The impact of corporate social responsibility (CSR) on FRQ evidence from european blue chips. Working Paper, Leipzig Graduate School of Management.

Scherer, A. G., & Palazzo, G. (2008a). Handbook of research on global corporate citizenship. Cheltenham: Edward Elgar.

Scherer, A. G., & Palazzo, G. (2008b). Globalization and corporate social responsibility. In A. Crane, A. McWilliams, D. Matten, J. Moon, & D. S. Siegel (Eds.), The Oxford handbook of corporate social responsibility (pp. 413–431). Oxford: Oxford University Press.

Schonrock-Adema, J., Heijne-Penninga, M., Van Hell, E. A., & Cohen-Schotanus, J. (2009). Necessary steps in factor analysis: Enhancing validation studies of educational instruments. Medical Teacher, 31, e226–e232.

Scott, R. W. (2012). Financial accounting theory (4th ed.). Canada: Pearson.

Tabachnick, B. G., & Fidell, L. S. (2001). Using multivariate statistics (4th ed.). Boston: Allyn and Bacon.

Webley, S., & Hamilton, K. (2004). How does business ethics pay? In The ISBEE conference, Melbourne, Australia, Institute of business ethics, London.

Acknowledgments

The authors would like to thank participants at the 2014 CAAA conference for helpful comments. We also appreciate helpful suggestions from the ASAC 2014 conference participants and thank them for choosing our research to be the Best Paper Award winner in accounting. We also thank the anonymous referee and the section Editor, Markus Milne for their valuable comments and suggestions. Finally, the authors acknowledge that partial funding for this project has been provided by the Institute for International Issues in Accounting (IIIA).

Author information

Authors and Affiliations

Corresponding author

Appendix

Rights and permissions

About this article

Cite this article

Elayan, F.A., Li, J., Liu, Z.F. et al. Changes in the Covalence Ethical Quote, Financial Performance and Financial Reporting Quality. J Bus Ethics 134, 369–395 (2016). https://doi.org/10.1007/s10551-014-2437-8

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10551-014-2437-8