Abstract

Research in recent years suggests that fairness concerns could mitigate hold-up problems. In this study, we report theoretical analysis and experimental evidence on an opposite possibility: that fairness concerns could also induce hold-up problems. In our setup, hold-up problems will not occur with purely self-interested agents, but theoretically could be induced by demand for distributional fairness among agents without sufficiently strong counteracting factors such as intention-based reciprocity. We observe a widespread occurrence of hold-up in our experiment. Relationship-specific investments occurred less than half of the time, resulting in significant inefficiencies. Moreover, whenever a relationship-specific investment was made: (a) it was typically not reciprocated by the partner; (b) nor did the investor’s offers at the bargaining stage exhibit expectations for reciprocity. Consequently, the partner extracted all the additional expected payoff from relationship-specific investments. Further experimentation suggested that our results were driven by a fundamental lack of intention-based reciprocity in fairness concerns, rather than self-serving bias.

Similar content being viewed by others

1 Introduction

Relationships often improve in value when the parties involved make relationship-specific investments. However, a common dilemma for the potential investor is whether the partner would take up all or most of the gains resulting from the investment, leaving the investor with no benefits in the end. If this is highly likely, the potential investor would be reluctant to invest. This, in essence, is the hold-up problem, which could result in significant inefficiencies.

Hold-ups are a prevalent concern when ex-ante contracts are incomplete and ex-post negotiations are not preventable (e.g., Grossman & Hart, 1986; Hart & Moore, 1990; Williamson, 1975, 1979, 1983).Footnote 1 In the traditional setup of these problems, underinvestment and inefficiencies occur due to potential self-interested expropriation by the relationship partner at ex-post negotiation. The embedded assumption of pure self-interest maximization has been questioned in a growing stream of research (see Kőszegi, 2014, for a broad overview of related topics), which provides theoretical and experimental evidence that hold-up can be mitigated by social preferences over fair dealings. A recent example is Haruvy et al. (2019), who applied Bolton and Ockenfels (2000)’s model of distributional fairness to a supply chain setting with hold-up problems, and demonstrated both theoretically and experimentally how the problems could be resolved by fairness concerns. More specific key issues that have been investigated include how fairness norms that have been established ex-ante can have a behavioral influence ex-post. The establishment of such norms can happen through contracting (Bartling & Schmidt, 2015; Fehr et al., 2011, 2015; Hart & Moore, 2008; Hoppe & Schmitz, 2011), communication (Charness & Dufwenberg, 2006; Ellingsen & Johannesson, 2004a, 2004b), or sunk cost effect (Carmichael & MacLeod, 2003). Complementing these studies, von Siemens (2009) and Dufwenberg et al. (2013) highlight how hold-up can be mitigated if agents who behave unfairly ex-post are liable to be punished effectively, even if the punishment is costly to the punisher.

In this article, we propose a starkly opposite possibility: that fairness concerns can also induce a hold-up problem and thus significant inefficiencies. We report theoretical analysis and experimental evidence of hold-up in scenarios in which hold-up will not occur if agents are purely self-interested but could occur if they care about fairness at ex-post negotiation. Our investigation is motivated by real-life concerns in a wide range of scenarios. For example, an employer might refrain from investing in production technology, because of the fear that employees might then demand a “fair” share of the increased value of the business (with the threat of mutually damaging industrial actions) that renders the original investment unprofitable. A manufacturer might also refrain from investing in customized service efficiency for a business customer, if there is fear that the latter would demand a high share of the increased value of the business for fairness’ sake, to the extent of allowing bargaining to break down in a mutually damaging fashion. A similar conundrum could be faced by a nation deciding whether to invest in an international trade agreement. The nation might decide not to invest, fearing that partnering nations would disregard its investment in their demand for fair deals in future negotiations. A similar situation may occur with environmental pledges: less developed nations may be reluctant to invest in green technologies if they believe that developed nations have strong demand for distributional fairness in terms of sharing the cost of carbon offset.

Such decision contexts imply a potential conflict between the demand for distributional fairness and positive reciprocity. The partner’s demand for distributional fairness (inequity aversion) would increase the minimum acceptable amount that is offered to them. However, the partner might also harbor positive reciprocity toward the investor’s earlier decision to invest in the relationship, which might then decrease their minimum acceptable amount. If inequity aversion dominates and undermines positive reciprocity, that is, when the partner’s social preference undervalues the past, then a hold-up problem could be induced by demand for fairness.

Previous studies of social preference have not fully addressed these situations. The literature on inequity aversion either focuses solely on the distribution of value as a utility component (Fehr & Schmidt, 1999), or studies trust and reciprocity as an indirect outcome of concerns for distributional fairness (Bolton & Ockenfels, 2000; Charness & Rabin, 2002). Meanwhile, another literature that focuses more specifically on trust and reciprocity typically leaves distributional fairness issues aside (e.g., Cox et al., 2007; Dufwenberg & Kirchsteiger, 2004; Falk & Fischbacher, 2006; Rabin, 1993).

Research on different fairness ideals, such as Cappelen et al. (2007), provides a different perspective. In the framework of Cappelen et al., libertarianism would be highly conscious of the relationship between investment and fairness; by contrast, strict egalitarianism would consider distributional fairness without regard to previous investments; liberal egalitarianism would have a more intermediate position. However, that line of research has so far not considered the strategic concerns in ex-post negotiation, which is central to hold-up problems and this study.

In the next section (Sect. 2), we present and analyze a theoretical model on which our experiment is based. In the model, hold-up does not occur with self-interested agents but theoretically could occur under inequity aversion regarding distributional fairness. We also observe that a sufficient level of intention-based reciprocity might mitigate the hold-up problem. We then report in Sect. 3 a laboratory experiment (Experiment 1) that provided empirical evidence for hold-up induced by demand for fairness. As it appears, inequity aversion dominated over any positive reciprocity in the partners’ decisions in our experiment. Accordingly, we observe a widespread occurrence of hold-up in our experiment. Relationship-specific investments occurred less than half of the time, resulting in significant inefficiencies. Moreover, whenever a relationship-specific investment was made: (a) it was typically not reciprocated by the partner, and (b) nor did the investor’s offers at the bargaining stage exhibit expectations for reciprocity. Consequently, on average, the partner extracted all the additional expected payoff from relationship-specific investments. We next report in Sect. 4 another experiment (Experiment 2) that was designed to investigate whether the apparent lack of positive reciprocity in the experiment was due to: (a) self-serving bias from the partner’s own egocentric perspective (Knez & Camerer, 1995), or (b) a more fundamental lack of intention-based reciprocity in this context that would apply to a neutral observer. The evidence from the second experiment points to the latter. Finally, in Sect. 5, we offer a concluding discussion and point out the limitations of our research as well as potential future directions.

2 Model and analysis

In this section, we describe and analyze a simple model that illustrates how a hold-up problem can be induced by the demand for fairness. Our model is based on inequity aversion with regard to distributional fairness.

2.1 Basic setup

Consider the following game with three periods and two agents, Player P and Player R (the players correspond to the investor and the partner, respectively, in the previous discussion). In period 1, Player P selects one out of a set of two ultimatum bargaining games, Game NI and Game I (“NI” stands for “not invest” and “I” stands for “invest,” as will be explained further). Game j (j \(\in\in\){NI, I}) can be described by the ordered pair (Mj, Cj), where Mj > 0 is the total amount to be allocated (the pie size) and Cj ≥ 0 is the outside option the proposer receives should the responder reject the proposer’s offer (see, e.g., Knez & Camerer, 1995, and Schmitt, 2004, for previous studies on ultimatum games with outside options). For simplicity, the responder’s outside option is zero in both games.

In periods 2 and 3, the two players play the game chosen by Player P in period 1, with Player P in the role of proposer and Player R in the role of responder. Specifically, if Game j is played:

-

(i)

In period 2, Player P offers to Player R an allocation such that Player R is allocated yj \(\in\in\) [0,Mj] and Player P allocates Mj-yj to themself;

-

(ii)

In period 3, Player R makes a binary decision to accept or reject Player P’s offer. If Player R accepts, the game ends with Player P earning a pecuniary payoff of Mj–yj and Player R earning a pecuniary payoff of yj. If Player R rejects, the game ends with Player P earning a pecuniary payoff of Cj and Player R earning a pecuniary payoff of zero. It is important to emphasize that these payoffs are pecuniary, which can be different from utilities after incorporating social preference.

The four parameters of the two games are common knowledge to both players. We further assume that MI > MNI > CNI > CI ≥ 0. That is, Game I has a larger pie size than Game NI, but Player P has a larger outside option in Game NI than in Game I; moreover, the outside option in Game NI is less than the pie size in either game. Therefore, Player P’s choice in period 1 between Game NI and Game I is equivalent to a relationship-specific investment, through which Player P sacrifices part of their outside option in return for an increase in the total amount to be allocated.

We next present two levels of analysis on possible decisions of players in the model, one under standard assumptions of self-interest, the other incorporating fairness concerns. As we can see, the two sets of analyses could result in completely opposite conclusions in payoffs and efficiencies.

2.2 Decisions under pure self-interest

If it is common knowledge that both players are purely self-interested in pecuniary payoffs, Player R will accept any minimal positive offer in period 3, so that Player P can keep virtually all of the value of the pie Mj to themself and should propose a corresponding allocation in period 2 to maximize self-interest. This implies that Player P will choose Game I in period 1 which does enhance the value of the relationship. This subgame perfect equilibrium does not incur a hold-up problem: Player P always invests in the relationship in equilibrium, thus guaranteeing full efficiency. Player P, moreover, is able to extract all the surplus from the investment.

2.3 Decisions with fairness concerns

If Player R has a social preference in the form of inequity aversion, so that they could reject positive offers that are too low and deemed too unfair relative to what Player P would gain, the picture could be very different.Footnote 2 Player P might then make a significantly positive offer to Player R in either game, to secure acceptance of offer.

We employ Fehr and Schmidt (1999)’s model of inequity aversion to obtain further results. Suppose Player P believes Player R’s preferences to be such that, if the payoffs to Player P and Player R are xP and xR, respectively, then Player R’s utility vR is:

where the two parameters αR and βR are such that αR ≥ βR and 1 > βR ≥ 0. The parameter αR characterizes Player R’s aversion to having less payoff than Player P (disadvantageous inequality), while the parameter βR characterizes Player R’s aversion to having more payoff than Player P (advantageous inequality).

Assume that Player P does not consider offers that would result in Player R earning more than Player P (this would be in line with empirical observations, and is also valid when Player P themselves have a Fehr-Schmidt utility function). If Player R is willing to accept an offer yj in Game j, so that the payoffs to the two players are Mj − yj and yj, then vR = yj − αR(Mj − 2yj); if Player R rejects that offer, so that the payoffs to the two players are Cj and 0, then vR = − αRCj. Hence, Player R accepts an offer in period 3 only if:

Since αR/(1 + 2αR) is not more than 1/2 by definition of the parameter αR, Player R’s minimum acceptable offer would not be more than half of the pie size in surplus of the outside option. Hence a pecuniary payoff-maximizing Player P should offer αR(Mj-Cj)/(1 + 2αR) to Player R in period 2 and keep the remainder of the pie, which is:

This is Player P’s subgame perfect equilibrium payoff in the subgame beginning in period 2, conditioned on having chosen Game j in period 1.

Finally, Player P will choose Game NI in period 1 if:

In other words, Player P will choose not to invest in increasing the value of the relationship, if they believe that Player R’s demand for fairness is sufficiently high with respect to the efficiency-outside option tradeoff between Game NI and Game I captured by (MI − MNI)/(CNI − CI). The intuition is that, compared with Game I, the higher outside option in Game NI provides a stronger “bargaining chip” for Player P that could lower Player R’s minimum acceptable offer, namely αR(Mj − Cj)/(1 + 2αR). This appeal of Game NI needs to be overturned by the appeal of Game I having a larger pie to split, in order for Player P to invest; otherwise, Player R’s demand for fairness (which would lead to rejection of perceived unfair offers) is effectively deemed too high to justify Player P’s investment, leading to a hold-up problem.

2.3.1 Incorporating uncertainty about the other player’s inequity aversion

The above analysis suffices in conveying our major insight that demand for fairness could create a hold-up problem. To tie in our analysis with experimental decisions, we now introduce an extension in which Player P is uncertain about Player R’s level of inequity aversion. Such uncertainty is manifested in a probabilistic belief about αR. To proceed, we first define σj = yj/(Mj − Cj), so that Player R accepts an offer only if σj ≥ αR/(1 + 2αR), which is equivalent to αR ≤ σj/(1− 2σj). Next, define p(σj) = Pr[αR ≤ σj/(1− 2σj)], a function of σj that is Player P’s subjective estimate of the probability that the offer will be accepted. Note that p(∙) is non-decreasing with p(0) = 0 and p(1/2) = 1. At the beginning of period 2, when Game j has been chosen to be played, an expected payoff maximizing Player P should make an offer that maximizes:

which is equivalent to choosing σj such that:

where the effective range of σ in the maximization problem is over 0 ≤ σ ≤ 1/2 because of the definition and properties of p(∙). As is also explicit in the above formulation, the maximization problem should yield the same optimal σj irrespective of the game, as p(∙) is a function of Player P’s belief over the distribution of αR only. In other words, we have σNI = σI = σ* upon Player P’s expected payoff maximization, and the inequality for hold-up becomes:

The intuition behind this hold-up condition is similar to that in the case without uncertainty but in a more general context. First, the left-hand side only depends on Player P’s belief over Player R’s Fehr-Schmidt inequity aversion coefficient αR and is independent of the right-hand side. Meanwhile, as in the case without uncertainty, we have a right-hand side that is a measure of the efficiency-outside option tradeoff between Game NI and Game I. If Player P believes that Player R has a sufficiently strong demand for fairness (i.e., p(σ*)(1- σ*) is sufficiently low) with respect to the efficiency-outside option tradeoff, then Player P would find it preferable not to invest, resulting in a hold-up problem.

Our experimental parameters involve a special case in which MI − MNI = CNI − CI, so that the decrease in outside option is equal to the increase in the pie size. The right-hand side is then equal to one, and hold-up occurs if p(σ*)(1 − σ*) < 1/2. Without uncertainty, so that Player P’s belief regarding αR is a single mass point distribution, σ* = αR/(1 + 2αR), p(σ*) = 1, p(σ*)(1 − σ*) = (1 + αR)/(1 + 2αR) > 1/2, and there would be no hold-up problem. However, with uncertainty, when Player P’s belief could be more diffuse, it is possible that p(σ*)(1 − σ*) < 1/2, when a hold-up would occur. For example, ultimatum game experiments (see, e.g., Camerer, 2003, Ch. 2.1) suggest that proposer offers are predominantly in the range of 30–50% of the pie size. If σ* = 40% for a Player P, then hold-up occurs when the player believes that their offer will be accepted with a probability that is less than 5/6 = 83%.

This special case highlights the more general implication that, when Player P is uncertain about Player R’s demand for fairness, so that Player P may entertain a more diffuse belief distribution for αR than the single mass point distribution in the case without uncertainty, the hold-up is correspondingly feasible over a larger range of (MI − MNI)/(CNI − CI). The intuition is that, under uncertainty, Player P typically cannot be sure whether an offer will be accepted or rejected. Thus, a higher outside option would serve the advantage of a better-guaranteed payoff in the event that the offer is rejected (in addition to providing a stronger “bargaining chip” that could lower Player R’s minimum acceptable offer with or without uncertainty). This then gives Player P more cause to choose a lower investment in return for a higher outside option.

2.4 Summary and discussion on other behavioral factors

To sum up our results in this section, investment in a relationship will always take place in our model if both agents are commonly known to be self-interested in pecuniary payoffs, and the investing agent will capture all the additional welfare from the investment. However, if agents have a social preference in the form of inequity aversion—to be more precise, if the investing agent believes that the other agent has inequity aversion—then a hold-up problem might occur. That is, the investing agent might shy away from investing to enhance the value of the relationship because a higher outside option could provide a stronger “bargaining chip” that could lower the other agent’s minimum acceptable offer. Moreover, hold-ups could be more widespread when the investing agent is uncertain about the other agent’s fairness demand since a higher outside option would then serve the additional advantage as a better-guaranteed payoff in the event that the offer is rejected.

Our analysis assumes that Player P believes that Player R is a Fehr-Schmidt decision maker. Moreover, we make the simplifying assumption that Player P is (expected) pecuniary payoff maximizing, which, in the present context, is consistent with Player P being a Fehr-Schmidt decision maker with negligible inequity aversion to earning a higher payoff than Player R. More relaxed assumptions, as well as other models of fairness concerns, could have been used. These other approaches would have yielded different parameter conditions for the occurrence of a hold-up problem induced by the demand for fairness but the present analysis suffices for our main objectives.

2.4.1 Intention-based reciprocity as a potential mitigating factor

An important issue is that we have not modeled any intention-based reciprocity in our theoretical analysis. As discussed conceptually in Sect. 1, reciprocity could be a mitigating factor in the occurrence of a hold-up in the present context.

More specifically, in our modeling analysis, Player R’s social preference in the ultimatum game in periods 2 and 3 is “blind” to the fact that Player P deliberately made a choice in period 1 of the game to be played in the next two periods. If, on the contrary, Player R’s decision in period 3 factors in Player P’s choice in period 1 over which game to play, Player R might exhibit positive reciprocity over and above the social preference that is analyzed in the present model. If Player P did choose Game I in period 1, Player R’s decision in period 3 may factor in reciprocating Player P having chosen a larger pie to divide between them. If Player R considers that Player P would have proposed a smaller allocation to Player R had Game NI been chosen, Player R might be especially inclined to exhibit positive reciprocity over and above the inequity aversion in the present model. Such an inclination could mitigate or even eliminate the hold-up problem discussed here.

For a simple illustration, consider the following modification of Player R’s utility vR in Game j upon being offered yj (based on Falk & Fischbacher, 2006’s theory):

If Player R accepts the offer, then vR = yj − αR(Mj − 2yj) + τR(j,yj) (Mj − yj − ERj(yj)),

If Player R rejects the offer, then vR = − αRCj + τR(j,yj) (Cj − ERj(yj)).

The terms that do not appear in the previous analysis are those with τR(j,yj), a function that captures the impact of Player P’s perceived “kindness” (from the perspective of Player R) in choosing Game j in period 1 and offering yj in period 2. ERj(yj) is Player R’s belief of Player P’s belief in the expected utility of offering yj in Game j, so that Mj − yj − ERj(yj) can be interpreted as the magnitude of the reciprocation (or “reciprocation term”) of Player R on Player P should Player R accept the offer. Likewise, Cj − ERj(yj) is the reciprocation term should Player R reject the offer. Consider “regular” offers yj that satisfy Mj − yj > Cj, i.e., the proposed offer will earn Player P more than their outside option. In addition, assume a simple, illustrative case where τR(I,yI) > 0 > τR(NI,yNI) whenever MI − yI = MNI − yNI, so that, controlling for the amount that Player P proposes to keep, Player R perceives Player P to be “kinder” if Player P chooses Game I than if Player P chooses Game NI. Then, for the same amount that Player P will earn from an accepted offer, the reciprocity terms will make acceptance more favorable to Player R in Game I and less favorable to Player R in Game NI, compared with when there is no reciprocity (i.e., τR(∙,∙) ≡ 0). If Player P believes that Player R will be affected by reciprocity in such a way, then Player P will be more likely to choose Game I.

Given that our modeling objective is to illustrate how a hold-up can be induced by demand for fairness, a full analysis of the impact of reciprocity is beyond the scope of this research. However, the factor can be present in real-life decisions and affect the descriptive validity of the analysis. Therefore, it is important to examine if real decision makers exhibit hold-up under a similar setting as our model—which is the objective of the experiments.

2.4.2 Sunk cost effect and anticipated regret as two potential contributing factors

In addition to the distributional fairness factor that is the central concern of this research, two other behavioral factors could potentially contribute to the occurrence of hold-up, in the sense of making Player P potentially more likely to not invest in period 1.

Sunk cost effect. If Player P invests, they would have forgone the higher outside option in Game NI in return for the lower outside option in Game I. This can potentially create a sunk cost effect (e.g., Arkes & Blumer, 1985; Carmichael & MacLeod, 2003) whereby, in period 2, Player P is not willing to offer an amount that does not “recoup” the sunk cost due to the difference in outside options between the Game NI and Game I. With respect to the earlier analysis without uncertainty, if the offer of [(1 + αR)Mj + αRCj]/(1 + 2αR) is not high enough to “recoup” the sunk cost for Player P, then there will be no possibility for an accepted split in period 2 and Player P will end up with the outside option CI. If Player P foresees this in period 1, Player P will not choose Game I in period 1, which again produces a hold-up scenario. Formally, if we express the sunk cost of choosing Game I for Player P as CNI − CI, then Player P should not choose Game I if:

This sets a different condition for the occurrence of a hold-up from what we have discussed. Note that, formally, the condition becomes CNI-CI > MI when αR → 0, which contradicts the basic model assumption that MI > CNI > CI. That is, sunk cost effect does not contribute to hold-up if Player R’s inequity aversion is sufficiently low – because Player P will then be able to claim a large enough portion of MI to “recoup” the sunk cost. On the other hand, the condition becomes 2CNI-3CI > MI when αR → ∞. In that case, as long as CNI-(3/2)CI ≤ 0 or the pie size of Game I is large enough vis a vis the difference in outside options, Player P will still be able to “recoup” the sunk cost in Game I and this factor will not contribute to the hold-up problem. To summarize, sunk cost effect will not exacerbate hold-up if Player R’s inequity aversion is sufficiently low or the pie size of Game I is large enough vis a vis the difference in outside options.

Anticipated regret. Another potential behavioral factor that might contribute to hold-up is anticipated regret (e.g., Bell, 1982; Loomes & Sugden, 1982). This is again related to the difference in outside options between the two games. Suppose Player P is considering whether to invest in period 1 and has an idea of what offer to propose should they choose Game I. If there is uncertainty regarding whether Player R will accept or reject that offer, then, in the event that the offer is rejected, Player P could experience regret over giving up a “safer” outside option in their choice of Game I. In anticipation of this regret, Player P may become less inclined to invest in period 1.

As an illustration of how this can impact Player P’s decision, we can model regret as a negative utility − λ(CNI − CI), where λ > 0, that is incurred if Player P chooses Game I in period 1 and then Player R rejects Player P’s offer in period 2. This modifies Player P’s expected utility in period 2 in Game I under the model in Sect. 2.3.1 to:

An application of the envelope theorem (with λ as the parameter of the optimization problem) leads to the conclusion that the optimized expected utility will be lower the higher the value of λ, meaning that anticipated regret will reduce the attractiveness of Game I, thus exacerbating hold-up. That said, this exacerbating impact will be very limited if Player P is highly certain about Player R’s inequity aversion, that is, if p(σj) is close to one in general.

As an endnote to the discussion on sunk cost effect and anticipated regret, we observe that these factors might contribute toward hold-up only if: (1) Player R has inequity aversion in the first place, and (2) Player P is able to factor in Player R’s inequity aversion in the period 1 decision (to be more precise, in the case of anticipated regret, Player P factors in the uncertainty about Player R’s inequity aversion in the period 1 decision). Hence, both factors affect hold-up in our analysis only insofar as the hold-up is induced by fairness concerns, as in our main findings.

3 Experiment 1

We next report an experiment designed to examine the existence of the hold-up problem discussed in the previous section. Our experiment follows our model setup and is in essence a modification of the ultimatum bargaining game, in which the proposer may make a relationship-specific investment by foregoing an outside option in return for an increase in the total amount to be allocated. The investment decision, therefore, involves a tradeoff between reduced protection (i.e. outside option) against prospective bargaining breakdown and an increase in the value of the relationship.

3.1 Procedure

Ninety-six subjects (including 58 males and 38 females; average age = 23.42) recruited from the experimental and behavioral economics subject pool of a UK university participated in the experiment. The experiment was conducted via an adaptation of the Qualtrics survey software on computer terminals. The main decision interfaces for both roles in the experiment (proposer and responder) can be found in Online Appendix A. Subjects’ earnings were contingent on their own decisions and the decisions of the subjects they were matched with to play the experimental games. Earnings were first calculated in the experimental currency, tokens, which were converted to real currency at the rate of £1 = 30 tokens at the end of the experiment. There was also a £2 show-up fee. Each experimental session lasted approximately half an hour, and the average payment per subject was £7.32 including the show-up fee.

Upon entering the laboratory, the subjects were first introduced to a version of the control game in the experiment (see below) for practice. Afterwards, they were informed about the role they had been assigned, upon which the main part of the experiment commenced.

Half of the subjects were randomly assigned to the role of the proposer (labelled as Participant P), the other half to the role of the responder (labelled as Participant R). For each role, the experiment had the same five conditions (called “tasks” in the experiment), including four control games and one focal game. Every subject was paid for their decision in the focal game plus one randomly selected control game. For each of these two games, payment was determined by independent random matching between proposers and responders. The random matching, and determination of payments, were carried out only after the experiment was over.

Each control game was an ultimatum game with a specific total amount to be allocated and an outside option for the proposer. Specifically, using the notation for the model in Sect. 2, the control games were (200 tokens, 0 tokens), (200 tokens, 40 tokens), (240 tokens, 0 tokens), (240 tokens, 40 tokens). The control games, therefore, formed a 2(total amount to be allocated: 200 tokens vs. 240 tokens) × 2(proposer’s outside option: 0 tokens vs. 40 tokens) within-subjects design; note that the responder’s outside option was always zero tokens. Specifically, each proposer was asked, for each control game, to indicate their proposed allocation of a number of tokens that was the bargained pie size, between themselves and the responder who would be randomly matched with them, had that game been randomly selected for payment. The possible allocations were constrained in our setup, so that offers to the responder were in multiples of 20 tokens, from zero tokens to the whole pie.

Meanwhile, for every allowed proposed allocation of tokens in every control game, each responder was asked whether they would accept or reject the allocation, had the proposer randomly matched with them made that offer.Footnote 3 Whichever the role, the decision tasks for the four control games were all listed within the same Qualtrics page and in the order (200,40), (200,0), (240,40), (240,0) (respectively, called Task 1 to Task 4 in the interface; see Online Appendix A). Subjects could scroll back and forth between the games as they made decisions.

Upon completing the four control games, subjects moved on to the focal game in a new webpage. The focal game was essentially the model developed in the previous section with Game NI being (200 tokens, 40 tokens) and Game I being (240 tokens, 0 tokens) (we would drop “tokens” in the subsequent discussion so that Game NI is (200,40) and Game I is (240,0)). Specifically, in the focal game, the proposer was first required to choose between two alternatives, Alternative A (corresponding to Game NI) and Alternative B (corresponding to Game I). If Alternative A was chosen, an ultimatum game would be played between the proposer and a matched responder with a pie size of 200 tokens and proposer’s outside option of 40 tokens. If Alternative B was chosen, an ultimatum game would be played between the proposer and the matched responder with a pie size of 240 tokens and proposer’s outside option of 0 tokens. While the proposers made the choice of alternative and then an offer in conjunction with that choice, each responder was asked to indicate their accept or reject decision contingent on each possible alternative and offer that could be chosen by the matched proposer. Subjects could also return to the page with the control games before finalizing their decision in the focal game.

Upon finalizing their decision in the focal game by clicking a forward button, subjects moved on to a new page for the final part of the experiment, during which they were provided an on-screen text box that prompted them to write down the rationale behind their decisions in the focal game. The text box prompt for proposers was: “What was your rationale behind your choice of Alternative (A or B) and your offer to Participant R?” while the text box prompt for responders was: “What was your rationale behind your decision on Participant P’s offer?”.

3.1.1 Further discussion on the design

Our experimental design allowed us to compare, for every subject, their decisions in the focal game with corresponding decisions in the control games. We also deliberately required subjects to play the control games first, so that they could familiarize themselves with the more basic ultimatum bargaining of the control games—which included the two alternatives in the focal game—before moving on to the more complex focal game. The order of the control games on their page was also the same across subjects to control for the familiarization experience. At the end of this section, we briefly describe follow-up sessions with the same subjects that involved the focal game without any control games, as a robustness test of our main results.

Another design feature that merits discussion is that the parameters of the focal game alternatives are such that MNI = 200, MI = 240, CNI = 40, and CI = 0 following the notation in Sect. 2. The proposer in the focal game is effectively faced with the decision of whether to “invest” the outside option of CNI = 40 in Alternative A (Game NI in the Sect. 2 analysis) to expand the pie by exactly that amount in Alternative B (Game I in the Sect. 2 analysis), i.e., increasing the pie from MNI = 200 to MI = 240. In return, the proposer “loses” the outside option of 40 as CI = 0. An interpretation of this decision is that investment in the focal game has a multiplier of one (formally (MI – MNI) / (CNI – CI)), since the “invested” outside option increases the pie by the same amount. This is a relatively low-efficiency game compared with, for example, the classic trust game (Berg et al., 1995), where the multiplier is three. This design feature is consistent with our research objective to find empirical evidence for the empirical possibility of hold-up induced by fairness concerns. As discussed in Sect. 2, intention-based reciprocity is a potential mitigating factor that prevents hold-up from being observed in an experiment like ours. Our focal game parameters in the experiment are therefore such that, while the game could still appear to be a non-trivial trade-off decision between efficiency and outside option, intention-based reciprocity was kept to a low level in the experiment.

3.2 Results

As discussed, the focal game involved a tradeoff for the proposer between giving up an outside option to increase the value of the relationship. We shall refer to a proposer who chose to not give up the outside option (i.e., Alternative A in the experiment, corresponding to Game NI in the model in Sect. 2) as a non-investor, while a proposer who chose to give that up (i.e., Alternative B in the experiment, corresponding to Game I in the model in Sect. 2) as an investor. We shall also refer to a proposer’s decision to choose Alternative B as investing.

The standard subgame perfect equilibrium argument, based on common knowledge of pure self-interest-maximization, predicts that the proposer should always be an investor in the focal game. Upon that choice, the proposer should offer the responder 20 tokens (the minimum positive amount that was allowed to be offered). The responder would accept the offer since it was higher than the payoff of 0 tokens in the case of rejection. The proposer would earn 220 tokens as a result, which would be strictly preferable to any outcome when the proposer did not invest.

On the contrary, in the context of our model in Sect. 2—which incorporates social preference in the form of inequity aversion regarding distributional fairness—we would expect that some proposers might not invest due to hold-up concerns. This would be especially the case if, as discussed in the Introduction section and at the end of Sect. 2, proposers did not expect significant positive reciprocity on the responders’ part that could mitigate the hold-up mechanisms behind our modeling analysis. In fact, if inequity aversion was a prominent factor while positive reciprocity was not expected by the proposers, we should see that the proposers often would not invest. Moreover, we should see that a proposer’s offers in the (240,0) ultimatum game in the experiment would be similar regardless of whether that game was a control game or chosen by a proposer to be played as part of the focal game; and likewise for the (200,40) ultimatum game. Meanwhile, if indeed responders did not exhibit significant positive reciprocity in the focal game, we should see that a responder’s decisions in response to offers in a specific ultimatum game such as (240,0) would also be similar regardless of whether that game was a control game or chosen by a proposer to be played as part of the focal game.

Accordingly, in the next three subsections, we examine three key types of variables in the experiment: (1) proposers’ investment decisions in the focal game, (2) proposers’ offers in the control as well as focal games, (3) responders’ acceptance thresholds (minimum acceptable offers, or MAOs) in the control as well as focal games, and (4) payoffs. We see that decisions clearly deviated from standard game-theoretic prediction, hold-up occurred, and subjects did not expect (in the case of proposers) or exhibit (in the case of responders) significant intention-based reciprocity.

3.2.1 Proposers’ investment decisions

Proposers’ investment decisions clearly contradicted the standard game-theoretic prediction based on self-interest maximization and were more consistent with our modeling analysis. Of the 48 proposers in Experiment 1, only slightly less than half of them (22 subjects, 45.83%) invested, while the remaining 26 subjects (54.17%) were non-investors. Thus, the total welfare of subjects in the experiment was strikingly lower than the maximum possible—which could be achieved only if all proposers invested. Seen in the context of our focal game being a simulation of our hold-up model, we conclude that:

Result 1. There is a significant existence of hold-up and inefficiencies in Experiment 1, as investments occurred less than half of the time.

The informal verbal comments collected at the end of the experiment shed light on the proposers’ decisions (see also Online Appendix B for the report of a supplementary content analysis). First, proposer subjects often deliberated carefully between the two alternatives in the focal game (e.g., “I felt (relatively) confident that a rational Participant R would accept any fair split of the money. Therefore, with Alternative A I thought I could get 100 tokens, but with Alternative B I could get 120 tokens. I opted for the one with more tokens.”). Moreover, subjects who did not invest (i.e., chose Alternative A in the focal game) largely saw it as a safer option with a higher guaranteed payoff (40 tokens) than if they invested (e.g., “I was guaranteed at least some tokens with Alternative A, even is Participant R rejected my offer.”). This line of thinking occurred even though, if those proposers modeled responders as self-interested maximizers of pecuniary payoffs, there should not be such a consideration. This suggests that the proposers were concerned with responders rejecting positive offers that were not deemed high enough. Meanwhile, proposers who invested showed high awareness of the responder’s demand for fairness (e.g., “I suppose they will accept my offer of sharing equally and with alternative B we can both get more money”). Their reasoning seemed to be that, even though they would have to make an offer that would be sufficiently fair—to make the offer likely to be accepted—investing would still yield them higher payoffs than otherwise. This is consistent with the strategic considerations analyzed theoretically in Sect. 2.

3.2.2 Proposers’ offers

Proposers’ offers again clearly contradicted the standard game-theoretic predictions. They were moreover in line with our modeling analysis without exhibiting any significant sign of expecting reciprocity on the responders’ part in the focal game.

Table 1 summarizes the observed proposer decisions in Experiment 1, expressed as offers to the responders and with a distinction between non-investors and investors. Specifically, we display the means and standard deviations, for every control game and each choice of alternative in the focal game, the proposer’s offer in a number of tokens, as a percentage of the total amount to be allocated (the pie size, Mj, using the notations in the theory section), and as a percentage of (Mj − Cj), the pie size in surplus of the outside option.

The offers were clearly higher than the standard game-theoretic prediction of the minimum positive amount allowed (20 tokens). This deviation is as we would expect in typical ultimatum games. More importantly for our study, there were no significant differences in offers between the control game (200,40) and its counterpart among the focal game alternatives, and similarly between the control game (240,0) and its focal alternative counterpart: paired t-test comparisons in both cases yielded p > 0.4. Among the non-investors, 15 subjects (57.69%) made the same offer in the control and focal (200,40) games; among the investors, 17 subjects (77.27%) made the same offer in the control and focal (240,0) games. Correspondingly, in the scatter plot in Fig. 1, the data points cluster about the 45-degree line but with small fluctuations above and below it for both investors and non-investors. The correlations between focal and corresponding control offer were 0.86 for non-investors and 0.90 for investors, respectively (p < 0.01 in both cases). Therefore:

Scatter plot of proposers’ percentage offers to responders in focal game vs. corresponding control game in Experiment 1. Pie size is the total number of experimental tokens allocated in the ultimatum game. For Alternative A (the choice of non-investors) in the focal game, it is 200 tokens; for Alternative B (the choice of investors), it is 240 tokens. The corresponding control game is the control game with the same parameters as the alternative chosen by the proposer in the focal game. Thus, the corresponding control game is (200,40) for non-investors and (240,0) for investors. As there are some overlapping data points, the plot is in bubble format where the area of each bubble is weighted by the number of data points (at most three in any bubble in the plot) it represents

Result 2. In Experiment 1, the proposers’ offers in their chosen focal game alternative were similar to those in the corresponding control game.

This result in particular means that the offers of investing proposers did not exhibit expectations of reciprocity (which would have made the offers more stringent than in the comparable control condition). Furthermore, among the control games, as indicated in Table 1, the proposer offered significantly less when there was an outside option of 40 tokens, compared with when there was not, controlling for the pie size. The proposer was obviously aware of the outside option’s influence on the responder’s demand for fairness (see below). The variations could be understood when the offers are expressed as percentages of Mj − Cj, the pie size in surplus of the outside option; as shown in Table 1 and supported by statistical analysis, when expressed in this way, the effects of the outside option on the offers went away (p > 0.1 in all relevant paired t-tests).

The observation carries over to the focal game as well. For example, as percentages of the surplus, the offers were on average 43.27% for non-investors playing (200,40) and 41.67% for investors playing (240,0) in the focal game. Between-subjects t-test yielded a non-significant difference (p > 0.7). Note that such a test potentially violates the independence of data points, as the proposers self-selected into non-investors and investors. Thus, we re-analyzed the focal game offer data using a sample selection model (see, e.g., Nakosteen & Zimmer, 1980). Specifically, we first modeled the proposer’s investment decision as a probit binary choice. We then modeled the subsequent offer decision, given either of the two investment decisions, as two linear regression models with normally distributed random errors that might correlate with the error term of the probit binary choice model. Our aim was primarily to check endogeneity, so all three models had only intercept terms. Our analysis showed that the correlation between each linear regression model error term and the probit model error term was non-significantly different from zero (p > 0.9). Hence we conclude that the between-subjects t test comparisons of offers between non-investors and investors were valid.

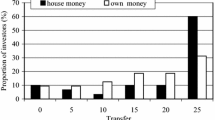

3.2.3 Responders’ minimum acceptable offers (MAOs)

As with the proposers’ investment decisions and offers, responders’ decisions also clearly contradicted the standard game-theoretic predictions. They also vindicated the proposers’ apparent lack of expectation of reciprocity: the responders did not exhibit any significant sign of reciprocity in the focal game.

Of the 48 responders, 45 (93.75%) exhibited normal monotonic preference in the sense that, in every game in the experiment, they accepted an offer as long as the offer was sufficiently high. The remaining three subjects (6.25%) rejected offers that were either too low or too high in every one of the five games (the second threshold being always higher than half of the total pie size). In all observations, it was always possible to define an unambiguous minimum acceptable offer (MAO). We shall focus our analysis on the MAOs in the data and report calculations based only on the MAOs; incorporating the more atypical decision strategies of the three plateau players in our analysis does not alter our major conclusions.

Table 2 and Fig. 2 summarize our findings for the responders. There were no significant differences in mean MAOs (in a number of tokens) between the control game (200,40) and its counterpart among the focal game alternatives, and similarly with the control game (240,0) and its focal alternative counterpart; paired t-test comparisons in both cases yielded p > 0.5. A consistent picture emerges from the very similar distributions of MAOs within each panel in the histograms in Fig. 2. In fact, 38 subjects (79.17%) prescribed the same MAO over the two (200,40) games, and 35 subjects (72.92%) prescribed the same MAO over the two (240,0) games. Correspondingly, the correlations between focal and corresponding control game MAOs were 0.90 for (200,40) and 0.88 for (240,0), respectively (p < 0.01 in both cases). That is:

Histograms of minimum acceptable offers of responders in Experiment 1. One subject indicated a high MAO of 220 in the focal game alternative (240,0) presumably based on the following view expressed in their informal verbal comment at the end of the experiment: “In the study where no one gained or lost tokens by rejecting an offer, I decided that I would reject all offers until I was in the best possible situation.” Another subject indicated a high MAO of 140 in the control game (240,0); the subject expressed a tradeoff between profit maximization and demand for fairness in their verbal comment: “I want to maximize my profits, but at the same time I would not accept offers where the allocation is very unfavorable for me”, but otherwise it is not clear why they indicated such a high MAO. All other MAOs were not more than half of the total amount allocated

Result 3. In Experiment 1, the responders’ minimum acceptable offers in each focal game alternative were similar to those in the corresponding control game.

In the informal verbal comments (see also Online Appendix B for the relevant results from our supplementary content analysis), the responders often did not consider the proposer’s endogenous choice between the two alternatives in the focal game. One subject explicitly mentioned that they ignored that choice and made decisions only in response to the amount of the offer: “Chose based only on the payoff to me at that stage of the game (ignored alternative stages …), ignoring payoff to Participant P.” It seems that responders were aware of the proposer’s choice of alternatives in the focal game, but considered each alternative, once chosen, in the same standalone context as the control games.

Our content analysis (see Table A1 in Online Appendix B) suggests that half of the subjects mentioned their willingness to accept any positive offer, with acknowledgement of the proposer’s bargaining position (e.g., “I was looking out for personal gain completely disregarding what Participant P would win or not. Since Participant P has the negotiating power, anything that was more than 0 for me was a benefit.”). This is reflected in the modes in the histograms in Fig. 2 being consistently at 20 tokens (with 30–35% of subjects choosing 20 tokens as MAO across the games represented). However, a considerable number of subjects also mentioned fairness of split as a criterion (e.g., “Decision made based on equal mutual benefits.”), as well as the intention to punish the proposer who offered too little (e.g., “I do think that Participant P should be offering *something* in my best interests for me to take the offer, and rejecting everything on the level and beneath that is a form of punishment.”). For Alternative A, the focal game alternative that would be played if the proposer decided not to give up the outside option, some subjects used that outside option (40 tokens) as a reference point for their MAOs (e.g., “In conditions where P would be paid 40 if I rejected, I wanted 40 or more before I would accept.”).

Another major observation is that the responders had significantly lower MAOs as percentages of the pie size when the proposer had the outside option of 40 tokens. As displayed in Table 2, these were typically 25–28% when the proposer had the outside option, and 21–22% otherwise, with statistical evidence as indicated in the table (paired t-test between the control games of (200,40) and (240,0) yielded p < 0.05 as well). The variations could be understood when the MAOs are expressed as percentages of the amount allocated in surplus of the outside option, as indicated in Table 2 and supported by statistical analysis (p > 0.8 in relevant paired t-tests for the effects of the outside option). That is, across different games, responders’ MAOs were consistently a similar percentage of the surplus. Such an interpretation is in line with Sect. 2.

Finally, consistent with the analysis of decisions in the experiment, we also find that subjects’ expected payoffs in a specific ultimatum game did not differ according to whether the game was a control game or chosen by the proposer to be played in the focal game. See Online Appendix B for details of this analysis.

3.3 Summary and further discussion; follow-up experimental sessions

Our data analysis for Experiment 1 suggests that similar strategic considerations were played out in the experiment as in our modeling analysis, leading to the significant existence of hold-up. Importantly, we do not obtain any evidence of significant intention-based reciprocity in the focal game.

In fact, we can try to apply the results of the experiment to evaluate the inequality criterion of hold-up put forward in Sect. 2.3.1, namely p(σ*)(1 − σ*) < 1/2. To proceed, we first assume a representative offer (as a percentage of surplus value) of σ* = 0.4 (Table 1), and a representative acceptance probability of p(σ*) = 0.8 (Table A2 in Online Appendix B), as the optimized values of these quantities for an expected payoff maximizing proposer. Meanwhile, the parameters of the focal game are such that MNI = 200, MI = 240, CNI = 40, and CI = 0. Substituting these into the inequality p(σ*)(1 − σ*) < 1/2, we obtain 0.48 on the left-hand side. That is, the proposer would be almost indifferent between investing and not investing. Tie breakers for the investment decision could be due to a heterogeneous spread of proposer beliefs over the responders’ inequity aversion, which corresponds to a spread of σ* and p(σ*) around the above representative values. Or, tie breakers could be due to other relatively minor factors in utilities, such as the proposer’s aversion to advantageous inequality (see Fehr & Schmidt, 1999), or the proposer’s model of the responder having non-linear terms in payoff differences beyond the Fehr-Schmidt model (see, e.g., Loewenstein et al., 1989, and an application in Bellemare et al., 2008). These effects might have manifested like a random noise among our proposers, which would then correspond with our observation of approximately half of the proposers choosing each of these decisions.

3.3.1 Follow-up experimental sessions

In our design of Experiment 1, subjects always played the focal game at the end after the control games. This was to help subjects to be familiar with standard ultimatum games, including the two alternatives in the focal game, before moving on to the more complex focal game. The order of the control games was also maintained to be the same so as to control for the familiarization experience. The downside, however, was that a systematic behavioral spillover might occur across subjects, as subjects might carry over their decisions from the control games to the focal game.

To address this issue, we carried out a number of follow-up sessions as a robustness check for the results from Experiment 1. About two months after Experiment 1, we invited the subjects in the experiment to short (approximately 15 min-long) sessions in which they were asked to make the decisions in the focal game in the same role as they were previously assigned. Subject payment in the follow-up sessions included a show-up fee of £1 plus the payment from randomly matching proposers’ and responders’ decisions in the sessions to play the focal game. Eventually, 41 proposers and 40 responders (out of 48 in each case) returned for the follow-up sessions; the average payment per subject was £2.86 including the show-up fee.

Indeed, our major conclusions from Experiment 1 regarding proposers’ decisions and responders’ MAOs remained unchanged in the follow-up sessions. For example, less than half (19 subjects, 46.34%) of the proposers invested in the follow-up sessions, closely following the data from Experiment 1. Tables A3 and A4 in Online Appendix B present a summary of the results. The tables show that offers and MAOs for the (200,40) focal game alternative were largely the same as in Experiment 1, while those for the (240,0) focal game alternative were lower. While responders were less demanding in (240,0), proposers offered less at the same time, so that qualitatively the picture was similar to that in Experiment 1.

4 Experiment 2

As discussed at the end of Sect. 2, hold-up induced by demand for fairness might have been avoided had Player R (corresponding to the responder in Experiment 1) exhibited positive reciprocity toward Player I (corresponding to the proposer in Experiment 1)’s decision in the first period of the game. However, Experiment 1 demonstrated a widespread occurrence of the hold-up and we have not detected significant reciprocal behavior of responders toward the proposers’ investment decisions. That is, the responders exhibited a demand for fairness that traced insufficiently backwards to the proposer’s investment decision.

Why this lack of reciprocity? One possibility is that the responders “chose to forget the past” because otherwise they would have felt obliged to lower their demand for fairness. In other words, responders might have been influenced by a self-serving bias. Self-serving bias has indeed been observed in previous bargaining studies (e.g., Babcock & Loewenstein, 1997; Babcock et al., 1995, 1996; Charness & Haruvy, 2000; Hennig-Schmidt et al., 2013; Knez & Camerer, 1995). Such possibility prompted us to investigate whether responder behavior in Experiment 1 was driven by self-serving bias from the responder’s own egocentric perspective. Alternatively, our observations might have been driven by a more fundamental lack of intention-based reciprocity in fairness concerns among humans—so that even a neutral third party would not see reciprocity toward the proposer’s investment as an important normative factor in the responder’s decisions.

Hence, in Experiment 2, we asked subjects to indicate, as third-party, neutral observers, their ideas of “fair” allocation of value in the focal game alternatives in Experiment 1, and their corresponding control games. If the subjects in Experiment 2 exhibited significant awareness of reciprocity to proposer investment as part of their notion of fairness, then the responders in Experiment 1 might well have been affected by self-serving bias. Otherwise, the idea of a fundamental lack of intention-based reciprocity in fairness concerns might be a better approach to organizing our observations.

4.1 Procedure

Forty-two subjects (including 19 males and 23 females; average age = 24.40) from the same subject pool as Experiment 1 participated in Experiment 2; none of them participated in Experiment 1. Each subject was first given a brief outline of the ultimatum games in Experiment 1, described as an “earlier experiment,” followed by a practice task that was also similar to that in Experiment 1. Afterwards, the experiment moved on to its main section, with a Qualtrics interface that was very similar to the responder’s in Experiment 1 (see Online Appendix A), but including only the (200,40) and (240,0) control games, followed by the two focal game alternatives. Moreover, the subject was asked to “please indicate what a fair decision (Accept or Reject) by Participant R should be” for each presented offer in each game (the bold text is as appeared in the experiment).

In addition, every subject was provided an on-screen text box at the end of the experiment with the prompt to “please write down any comments regarding how you evaluated ‘fair decisions’” in the experimental task. As compensation, subjects were informed that three £50 Amazon gift vouchers would be given out via a prize draw among participants.

4.2 Results

Of the 42 subjects, 31 (73.81%) exhibited normal monotonic preference in the sense that, in every one of the four games in the experiment, they (as third-party observers) accepted an offer for the responder as long as the offer was sufficiently high. That is, they were consistently threshold players in the terminology of Bellemare et al. (2008). Of the remaining subjects, nine (21.43%) rejected offers that were either too low or too high in every game (the second threshold being always higher than half of the total pie size); those subjects were consistently plateau players as per Bellemare et al. The remaining two subjects accepted low offers but rejected high offers in at least some of the games, and none of them switched more than twice between accept and reject as the offer increased in any given game. In all observations, it was always possible to define an unambiguous MAO. We shall focus our analysis on the MAOs in the data.

Table 3 and Fig. 3 summarize our main findings. As it appears, even as third-party observers judging what fair decisions should be, subjects were consistently non-reciprocal toward the investor. There were no significant differences in mean MAOs (in number of tokens) between the control game (200,40) and its counterpart among the focal game alternatives, and similarly between the control game (240,0) and its focal alternative counterpart: paired t-test comparisons in both cases yielded p > 0.8. A consistent picture emerges from the very similar distributions of MAOs within each panel in the histograms in Fig. 3. In fact, 30 subjects (71.43%) prescribed the same MAO over the two (200,40) games, and 27 subjects (64.29%) prescribed the same MAO over the two (240,0) games. Correspondingly, the correlations between focal and corresponding control game MAOs were 0.82 for (200,40) and 0.88 for (240,0), respectively (p < 0.01 in both cases). To conclude:

Histograms of fair minimum acceptable offers for responders as prescribed by subjects in Experiment 2. One subject prescribed very high MAOs (140 in the (200,40) games and 220 in the (240,0) games) presumably based on the view, expressed in informal verbal comments at the end of the experiment, that “Participant R has the bargaining power in this situation” so that the proposer should only be able to earn an amount that was just higher than their outside option. All other subjects prescribed MAOs that were not more than half of the total amount allocated

Result 4. In Experiment 2, the “fair” minimum acceptable offers in each focal game alternative were similar to those in the corresponding control game.

The informal verbal comments collected at the end of the experiment include some elaborately spelled out views of fairness regarding the games (see also Online Appendix B for the relevant results from our supplementary content analysis). Those views were highly heterogeneous: some subjects considered any positive offer to be fair (e.g., “I judged fair as both participants gaining something more than the benefit of rejecting the decision.”), while some saw fair offers as only offers resulting in an equal split of the pie (e.g., “I just thought Participant R should accept any amount of money that's the same as Participant P or over the amount.”). Only one subject raised a comment regarding reciprocity toward the proposer’s choice in the focal game, and that comment was framed in the spirit of negative reciprocity, that is, the proposer should be punished for not choosing the (240,0) alternative: “When P had the choice I felt that it was greedy/sneaky of them to go for option A, so I punished them by rejecting better deals. Yet if they chose B I felt that there were more tokens to go round so they ought to offer more.”

The concern for distributional fairness among subjects was reflected in the histograms in Fig. 3 being much more centered around higher offers than the corresponding ones for Experiment 1 in Fig. 2. We also observe that the MAO as a percentage of the pie size was on average not significantly different across games (p > 0.4 in all paired t-test comparisons) and was consistently around 30–32%. This implies that, as a percentage of the surplus over the outside option, the mean MAO was significantly higher in the (200,40) games than in the (240,0) games, as is also indicated in Table 3 with statistical evidence. These results are markedly opposite from the corresponding ones in Experiment 1. In Experiment 1, with a real payoff at stake, the responders were often more concerned with pecuniary self-interest than with fairness and were more sensitive to the outside option (if any) as a bargaining advantage of the proposer. As a result, in contrast with the subjects in Experiment 2, the responders in Experiment 1 exhibited lower MAO as a percentage of the pie size in games in which the proposer had the outside option of 40, but similar MAOs across games as a percentage of the value in surplus of the outside option.

An important upshot is that, if the allocation of values in the focal game was left to the jurisdiction of the third-party subjects in Experiment 2, the proposers would benefit from investing, as their payoffs would be significantly higher (see the last row in Table 3) when the value of the relationship was enhanced under investment. This was due to: (a) Experiment 2 subjects’ consistent application of proportional split of the pie across games, and (b) if allocation was really left to third-party jurisdiction, there would be no issue of bargaining breakdown. Meanwhile, in Experiment 1, with the acceptance rate being considerably less than certain, and the responder indicating lower MAO when the proposer had an outside option of 40, the proposer’s expected payoffs were not significantly different across the focal game alternatives.

5 Concluding remarks

The present research is a novel attempt in investigating, in a single study and both theoretically and experimentally, whether social preferences can cause hold-up problems. In identifying a causal link between fairness concerns and hold-up, we contribute to the studies of both social preferences and incomplete contracts. Our contributions have been supported by theoretical analysis as well as experimental evidence. It is important to re-emphasize that the hold-up problem we study is driven, as opposed to mitigated (as studied in previous literature), by social preference. In our setup, the existence of demand for fairness could be strong enough to induce a hold-up where there would have been none, had there been no social preference at all.

We also contribute to the study of social preferences by highlighting a scenario in which demand for distributional fairness potentially conflicts with reciprocating tendencies; our experimental evidence suggests an overwhelming dominance of the former over the latter. It is true that humans have a general capacity to reciprocate positively, as demonstrated by trust game experiments from Berg et al. (1995) onwards. Further results such as Cox (2004) established the independence of reciprocity from social preferences for distributional fairness; studies such as Gneezy and List (2006) established the impact of reciprocity on economic activities in the field. While acknowledging these facts, what we have demonstrated is that reciprocity might trace insufficiently backwards over a history of actions, so that it cannot remedy hold-up induced by current distributional fairness demand.

In fact, in our data for Experiment 1, we have not detected any significant positive reciprocal behavior of the responders toward the welfare-enhancing actions of investing proposers. Moreover, only responders benefited significantly from an investment, in terms of expected payoffs in the experiment. Accordingly, in Experiment 1, only 46% of the proposers invested in the relationship; the widespread underinvestment empirically presented a hold-up problem.

In Experiment 2, subjects as third-party observers largely considered any controlled game and its corresponding focal game alternative in the same manner, as far as “fair” minimum acceptable offers were concerned. Thus, there is no evidence that insufficient reciprocity toward the investing party in Experiment 1 was due to self-serving bias. The phenomenon seemed to be the result of a fundamental lack of intention-based reciprocity in fairness concerns. Previous studies such as Hoppe and Schmitz (2011) and Bartling and Schmidt (2015) suggest how fairness, as a norm, is susceptible to historical reference point effects to the extent of mitigating hold-up. Our observations do not contest these findings. Rather, our objectives pertain to historical actions that contributed to current welfare, rather than historical reference points per se, and we find that the historical actions in our settings had a non-significant influence on the current fairness norm. It thus appears that decisions across both experiments fit Cappelen et al. (2007)’s description of strict egalitarianism better than the other types of fairness ideals that they proposed.

5.1 Limitations

As discussed in Sects. 2.4.1 and 2.4.2, there are additional behavioral factors that might mitigate (e.g., intention-based reciprocity) or reinforce (e.g., sunk cost effect and anticipated regret) the hold-up problem that we investigate. While we have offered simple analytical illustrations of them, we have not conducted a more comprehensive theoretical analysis of the interaction of these factors that might help us to further understand the behavioral underpinnings of our data. That said, the analysis of verbal comments has not detected a significant presence of any of these additional factors (see Table A1 in Online Appendix B).

Another notable point is that the proposer had no outside option (CI = 0) in the alternative with investment, which is a boundary scenario in terms of the parameters. In practice, such as in the examples mentioned at the beginning of this article, both the investing and responding parties may have some bargaining power in the form of outside options. Those scenarios might be better modeled as having interior parameters in the sense of both parties having positive outside options.

With respect to Experiment 2, our survey-based method of collecting fairness-related data was non-incentivized. Instead, it might have been possible to use an incentivized elicitation approach such as Krupka and Weber (2013)’s coordination game method to elicit subjects’ fairness norms.

5.2 Future directions

Our research can be extended in multiple directions. First of all, while our work points out how hold-up could be induced by fairness concerns, previous behavioral literature (as discussed earlier) has been concerned with how hold-up could be mitigated by fairness concerns. This suggests that a more comprehensive investigation could involve considering three possibilities: (1) the possibility that hold-up can occur even when agents have purely self-interested preferences; (2) under some conditions, social preferences can mitigate the hold-up problem; (3) under some conditions, social preferences can exacerbate the hold-up problem. An interesting question for further research pertains to the relationships between these conditions. Overall, it would be highly useful to study an environment in which all three possibilities can occur and interact and understand their implications. An interior choice of parameters, as discussed in the previous subsection on Limitations, might be appropriate for such further investigations. For example, a higher outside option for the proposer (Player P in the model) under the investing scenario, coupled with a higher multiplier (see Sect. 3.1.1) to make investment more efficient, might be able to trigger higher reciprocity and less likelihood of hold-up induced by fairness concerns. The following discussion provides some further suggestions.

Returning to the motivating examples at the beginning of this paper—be that labor, customer, or international relationships—it could be especially important to explore behavioral measures that could motivate reciprocity to mitigate the hold-up concerns investigated here. For instance, relationship-specific investment in our model and experiment is in the form of sacrificing outside option in return for an increase in the total amount to be allocated. If the investment is in the form of a direct sunk cost and framed clearly as such—which is a practically feasible approach—perceptions that this is an incurred loss may help to motivate reciprocity from the partner.

It should also be noted that, while reciprocity was not apparent in our experiments, it was manifested in standard trust games (e.g., Berg et al., 1995) in which the investment from the trustor directly became a gain for the trustee. As discussed in Sect. 3.1.1, our experimental design parameters were specifically chosen to make the impact reciprocity potentially less significant so as to make the hold-up problem we investigated more likely to be observed. The multiplier or (MI – MNI) / (CNI – CI) (following the notation in Sect. 2), which indicates the efficiency gain from investing vis a vis the amount of outside option that the proposer has to give up, was equal to one in our experiment. A higher multiplier could lead to reciprocity having a more significant impact—a possibility that could be explored in future studies. Moreover, if, in the context of our model and experiments, the investor could frame the bargaining proposal as splitting the gain in efficiency from the investment, the strategy might also be able to motivate reciprocity. That is, for example, separating the negotiation into two parts, one part being the division of the increase in 40 tokens in pie size from Game NI to Game I, the other being the division of the “original” pie of 200 token so that the partner could more clearly perceive that they are benefiting from the investment.

Another direction pertains to communication: if the investor can voice and defend their own contribution during bargaining, would that mitigate the insufficient intention-based reciprocity in the non-investors fairness concerns? Further, if the two parties could conduct pre-play communication, as has been researched in another stream of experimental studies on standard hold-up problems (see the introductory section), would that mitigate hold-up in our context too? And how would the impact of all these factors change in an ongoing, long-term relationship? The crux is that fairness concerns are highly and dynamically susceptible to contextual influences so that it would be an important next step to identify more of those influences that can mitigate the hold-up we observed.

Notes

The punishment in this context, which involves Player R sacrificing their own payoff, can be understood in terms of a preference for distributional fairness, or inequity aversion. Alternatively, it can be understood as negative reciprocity against being harshly treated, which is a different type of fairness concerns; see the related references cited later on in this section. Empirically, the rejection of positive offers in ultimatum games has been observed in decades of ultimatum game experiments (see the survey in Güth and Kocher, 2014), even under very stringent anonymity conditions (e.g., Bolton and Zwick, 1995).

This is the strategy method for eliciting responder strategies in ultimatum games, which has the advantage of allowing the experimenter to collect very comprehensive decision data. The method has been employed by, among others, Bellemare et al. (2008), who also offered a discussion (see footnote 4 of their article) on the empirical evidence regarding how the approach compared with collecting the responder’s decision only after revealing the proposer’s offer.

References

Arkes, H. R., & Blumer, C. (1985). The psychology of sunk cost. Organizational Behavior and Human Decision Processes, 35(1), 124–140. https://doi.org/10.1016/0749-5978(85)90049-4

Babcock, L., & Loewenstein, G. (1997). Explaining bargaining impasse: The role of self-serving biases. Journal of Economic Perspectives, 11(1), 109–126. https://doi.org/10.1257/jep.11.1.109

Babcock, L., Loewenstein, G., Issacharoff, S., & Camerer, C. F. (1995). Biased judgments of fairness in bargaining. American Economic Review, 85(5), 1337–1343.

Babcock, L., Wang, X., & Loewenstein, G. (1996). Choosing the wrong pond: Social comparisons in negotiations that reflect a self-serving bias. The Quarterly Journal of Economics, 111(1), 1–19. https://doi.org/10.2307/2946655

Bartling, B., & Schmidt, K. M. (2015). Reference points, social norms, and fairness in contract renegotiations. Journal of the European Economic Association, 13(1), 98–129. https://doi.org/10.1111/jeea.12109

Bell, D. E. (1982). Regret in decision making under uncertainty. Operations Research, 30(5), 961–981. https://doi.org/10.1287/opre.30.5.961

Bellemare, C., Kröger, S., & van Soest, A. (2008). Measuring inequity aversion in a heterogeneous population using experimental decisions and subjective probabilities. Econometrica, 76(4), 815–839. https://doi.org/10.1111/j.1468-0262.2008.00860.x

Berg, J., Dickhaut, J., & McCabe, K. (1995). Trust, reciprocity, and social history. Games and Economic Behavior, 10(1), 122–142. https://doi.org/10.1006/game.1995.1027

Bolton, G. E., & Ockenfels, A. (2000). ERC: A theory of equity, reciprocity, and competition. American Economic Review, 90(1), 166–193. https://doi.org/10.1257/aer.90.1.166

Bolton, G. E., & Zwick, R. (1995). Anonymity versus punishment in ultimatum bargaining. Games and Economic Behavior, 10(1), 95–121. https://doi.org/10.1006/game.1995.1026

Bolton, P., & Dewatripont, M. (2005). Contract theory. MIT Press.

Camerer, C. F. (2003). Behavioral game theory. Princeton University Press.

Cappelen, A. W., Hole, A. D., Sørensen, E. Ø., & Tungodden, B. (2007). The pluralism of fairness ideals: An experimental approach. American Economic Review, 97(3), 818–827. https://doi.org/10.1257/aer.97.3.818

Carmichael, L., & MacLeod, W. B. (2003). Caring about sunk costs: A behavioral solution to holdup problems with small stakes. Journal of Law, Economics, and Organization, 19(1), 106–118. https://doi.org/10.1093/jleo/19.1.106

Cason, T. N., & Mui, V. L. (2015). Rich communication, social motivations, and coordinated resistance against divide-and-conquer: A laboratory investigation. European Journal of Political Economy, 37, 146–159. https://doi.org/10.1016/j.ejpoleco.2014.10.005

Charness, G., & Dufwenberg, M. (2006). Promises and partnership. Econometrica, 74(6), 1579–1601. https://doi.org/10.1111/j.1468-0262.2006.00719.x