Abstract

In the theoretical description of prospect theory, distinct sets of parameters can control the curvature of the value function and the shape of the probability weighting function. There is one for the gain domain and one for the loss domain. However, in most estimations, behaviour over losses is assumed to perfectly reflect behaviour over gains, through a unique set of parameters. We examine the consequences of relaxing this simplifying assumption in the context of Tanaka et al.’s (Am Econ Rev 100(1):557–571, 2010) risk-elicitation procedure based on multiple price lists. We show that subjects’ behaviour for gains is mostly reflected for losses at the aggregate and individual levels, and is consistent with the distinctive prospect theory fourfold pattern. Reflection is only partial as the mean curvature of the value function is slightly less convex for losses than it is concave for gains. These results are robust to a high-stake context. However, we demonstrate that assuming reflection can have huge consequences on loss-aversion measures. Incidentally, we also highlight the existence of a strong, negative and persistent pure loss-frame effect on elicited loss aversion. We recommend that future practitioners and modellers are particularly cautious about the loss-aversion values they obtain or use because these are especially sensitive to parametric assumptions and framing.

Similar content being viewed by others

Availability of data and material

The experimental instructions used in this study are included in this article as supplementary material. The datasets generated and analysed during the current study are not publicly available due the fact that they constitute an excerpt of research in progress but are available from the corresponding author on reasonable request.

Code availability

The code used to analyse the datasets is available upon request.

Notes

Booij et al. (2010) and L’Haridon and Vieider (2019) are exceptions in this respect as they rely on certainty and/or probability equivalents, using a matching and a choice procedure, respectively. Choices made on random lottery pairs are another usual experimental design but they are more common for laboratory measures (e.g. Harrison & Rutström, 2009).

Non-parametric methods include Wakker and Deneffe’s (1996) trade-off method, taken further by Abdellaoui (2000), Abdellaoui et al. (2007) and Abdellaoui et al. (2016), and based on measurements of indifferences. They are typically more difficult to administer and may suffer from error propagation because of their chained nature (L’Haridon & Vieider, 2019). They are also generally less efficient because more questions are needed (Abdellaoui et al., 2008). Last, they were made incentive compatible only recently (Johnson et al., 2021). See Bauermeister et al. (2018) for a laboratory comparison of the TCN method with Wakker and Deneffe’s (1996) under the PT framework.

The implicit scaling convention for the value function is \(v(y=1)=1\) and \(v(y=-1)=-1\). When \(\sigma ^+\) and \(\sigma ^-\) are not the same, the power specification implies \(\lambda\) is defined relative to the unit of money used for the y outcomes (Wakker, 2010, pp. 267–268).

Let us assume the following value functions defined separately over the gain and loss domains: for \(y>0\), \(v(y) = y^a\) and, for \(y<0\), \(v(y) = -\lambda (-y)^b\), where \(\lambda >0\) is the coefficient of loss aversion and \(a \ne b\). Wakker (2010) recalls it implies there is always a part of the gain domain where \(v(y)>-v(-y)\). However, it is empirically plausible that \(v(y) \le -v(-y)\) for all \(y>0\).

See Wakker et al. (2007, p. 224) for additional studies with unclear or balanced findings.

Appendix C gives the distribution of subjects’ switching points in the baseline GLo treatment. Similarly to other TCN risk experiments carried out in rural areas (e.g. Tanaka et al., 2010; Bocquého et al., 2014), we find that students massively choose extreme switching points in all three series. The never switch option in Series 1 is an exception, though.

Wilcoxon signed-rank tests for matched pairs, which are the equivalent non-parametric tests, lead to the same conclusions with the same levels of significance (p-values of 0.032 and 0.000 for Series 1 and 2, respectively). It means the distributions of the total number of LHS choices among subjects are statistically different from each other between the gain and loss frames.

Wilcoxon signed-rank tests for matched pairs give similar conclusions about the distributions of the total number of LHS choices.

In the EU context, Reynaud and Couture (2012) replicate Holt and Laury’s (2002) as well as Eckel and Grossman’s (2008) baseline lotteries, and also multiply stakes by 20. They find that, for both methods, the mean constant relative risk aversion coefficients are statistically different, subjects being more risk averse for high payoffs than for low payoffs. However, in the case of Holt and Laury’s (2002) experiment, they report that distribution of the coefficients is not modified by the payoff level.

References

Abdellaoui, M. (2000). Parameter-free elicitation of utility and probability weighting functions. Management Science, 46(11), 1497–1512.

Abdellaoui, M., Bleichrodt, H., & L’Haridon, O. (2008). A tractable method to measure utility and loss aversion under prospect theory. Journal of Risk and Uncertainty, 36(3), 245–266.

Abdellaoui, M., Bleichrodt, H., L’Haridon, O., & van Dolder, D. (2016). Measuring loss aversion under ambiguity: A method to make prospect theory completely observable. Journal of Risk and Uncertainty, 52, 1–20.

Abdellaoui, M., Bleichrodt, H., & Paraschiv, C. (2007). Loss aversion under prospect theory: A parameter-free measurement. Management Science, 53(10), 1659–1674.

Andersen, S., Harrison, G. W., & Rutström, E. E. (2006). Choice behavior, asset integration and natural reference points. Working Paper 06-07, Department of Economics, College of Business Administration, University of Central Florida.

Attema, A. E., Brouwer, W. B. F., & l’Haridon, O. (2013). Prospect theory in the health domain: A quantitative assessment. Journal of Health Economics,32(6), 1057–1065.

Attema, A. E., Brouwer, W. B. F., l’Haridon, O., & Pinto, J. L. (2016). An elicitation of utility for quality of life under prospect theory. Journal of Health Economics,48, 121–134.

Attema, A. E. (2012). Developments in time preference and their implications for medical decision making. Journal of the Operational Research Society, 63, 1388–1399.

Babcock, B. A. (2015). Using cumulative prospect theory to explain anomalous crop insurance coverage choice. American Journal of Agricultural Economics, 97(5), 1371–1384.

Barberis, N. C. (2013). Thirty years of prospect theory in economics: A review and assessment. Journal of Economic Perspectives, 27(1), 173–196.

Barberis, N., Huang, M., & Santos, T. (2001). Prospect theory and asset prices. The Quarterly Journal of Economics, 116(1), 1–53.

Bauermeister, G.-F., Hermann, D., & Musshoff, O. (2018). Consistency of determined risk attitudes and probability weightings across different elicitation methods. Theory and Decision, 84, 627–644.

Bleichrodt, H., & Pinto, J. L. (2002). Loss aversion and scale compatibility in two-attribute trade-offs. Journal of Mathematical Psychology, 46(3), 315–337.

Bocquého, G., Deschamps, M., Helstroffer, J., Jacob, J., & Joxhe, M. (2018). Risk and refugee migration. Sciences Po OFCE Working Paper, no. 10, 2018-03-12.

Bocquého, G., Jacquet, F., & Reynaud, A. (2014). Expected utility or prospect theory maximisers? Assessing farmers’ risk behaviour from field-experiment data. European Review of Agricultural Economics, 41(1), 135–172.

Booij, A. S., & van de Kuilen, G. (2009). A parameter-free analysis of the utility of money for the general population under prospect theory. Journal of Economic Psychology, 30(4), 651–666.

Booij, A., van Praag, B., & van de Kuilen, G. (2010). A parametric analysis of prospect theory’s functionals for the general population. Theory and Decision, 68, 115–148.

Bosch-Domènech, A., & Silvestre, J. (2006). Reflections on gains and losses: A 2 \(\times\) 2 \(\times\) 7 experiment. Journal of Risk and Uncertainty, 33, 217–235.

Bosch-Domènech, A., & Silvestre, J. (2013). Measuring risk aversion with lists: A new bias. Theory and Decision, 75, 465–496.

Bouchouicha, R., & Vieider, F. M. (2017). Accommodating stake effects under prospect theory. Journal of Risk and Uncertainty, 55, 1–28.

Bougherara, D., Gassmann, X., Piet, L., & Reynaud, A. (2017). Structural estimation of farmers’ risk and ambiguity preferences: A field experiment. European Review of Agricultural Economics, 44(5), 782–808.

Campos-Vazquez, R. M., & Cuilty, E. (2014). The role of emotions on risk aversion: A prospect theory experiment. Journal of Behavioral and Experimental Economics, 50, 1–9.

Cohen, M., Jaffray, J.-Y., & Said, T. (1987). Experimental comparison of individual behavior under risk and under uncertainty for gains and for losses. Organizational Behavior and Human Decision Processes, 39(1), 1–22.

Csermely, T., & Rabas, A. (2016). How to reveal people’s preferences: Comparing time consistency and predictive power of multiple price list risk elicitation methods. Journal of Risk and Uncertainty, 53, 107–136.

Eckel, C. C., & Grossman, P. J. (2008). Forecasting risk attitudes: An experimental study using actual and forecast gamble choices. Journal of Economic Behavior & Organization, 68(1), 1–7.

Etchart-Vincent, N. (2004). Is probability weighting sensitive to the magnitude of consequences? An experimental investigation on losses. Journal of Risk and Uncertainty, 28(3), 217–235.

Fehr-Duda, H., Bruhin, A., Epper, T., & Schubert, R. (2010). Rationality on the rise: Why relative risk aversion increases with stake size. Journal of Risk and Uncertainty, 40, 147–180.

Fehr-Duda, H., de Gennaro, M., & Schubert, R. (2006). Gender, financial risk, and probability weights. Theory and Decision, 60, 283–313.

Fennema, H., & van Assen, M. (1998). Measuring the utility of losses by means of the tradeoff method. Journal of Risk and Uncertainty, 17, 277–296.

Grinblatt, M., & Han, B. (2005). Prospect theory, mental accounting, and momentum. Journal of Financial Economics, 78(2), 311–339.

Harbaugh, W. T., Krause, K., & Vesterlund, L. (2010). The fourfold pattern of risk attitudes in choice and pricing tasks. The Economic Journal, 120(545), 595–611.

Harrison, G. W., & Rutström, E. E. (2008). Risk aversion in the laboratory. In J. C. Cox & G. Harrison (Eds.), Risk aversion in experiments, research in experimental economics (Vol. 12, pp. 41–196). JAI Press.

Harrison, G. W., & Rutström, E. E. (2009). Expected utility theory and prospect theory: One wedding and a decent funeral. Experimental Economics, 12, 133–158.

Hershey, J. C., Kunreuther, H. C., & Schoemaker, P. J. (1982). Sources of bias in assessment procedures for utility functions. Management Science, 25(8), 936–953.

Holt, C. A., & Laury, S. K. (2002). Risk aversion and incentive effects. American Economic Review, 92(5), 1644–1655.

Johnson, C., Baillon, A., Bleichrodt, H., Li, Z., Dolder, D. V., & Wakker, P. P. (2021). Prince: An improved method for measuring incentivized preferences. Journal of Risk and Uncertainty, 62(1), 1–28.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263–291.

Köbberling, V., & Wakker, P. P. (2005). An index of loss aversion. Journal of Economic Theory, 122(1), 119–131.

Kühberger, A., Schulte-Mecklenbeck, M., & Perner, J. (1999). The effects of framing, reflection, probability, and payoff on risk preference in choice tasks. Organizational Behavior and Human Decision Processes, 78, 204–231.

Lau, M., Yoo, H. I., & Zhao, H. (2019). The reflection effect and fourfold pattern of risk attitudes: A structural econometric analysis. Department of Economics, Copenhagen Business School, and Durham University Business School, Durham University.

Laury, S. K. & Holt, C. A. (2008). Further reflections on the reflection effect. In J. C. Cox, & G. Harrison (Eds.), Risk aversion in experiments, research in experimental economics (Vol. 12, pp. 405–440). JAI Press.

L’Haridon, O., & Vieider, F. M. (2019). All over the map: A worldwide comparison of risk preferences. Quantitative Economics, 10, 185–215.

Liebenhem, S., & Waibel, H. (2014). Simultaneous estimation of risk and time preferences among small-scale cattle farmers in West Africa. American Journal of Agricultural Economics, 96(5), 1420–1438.

Liu, E. (2013). Time to change what to sow: Risk preferences and technology adoption decisions of cotton farmers in China. The Review of Economics and Statistics, 95(4), 1386–1403.

Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7(1), 77–91.

Mercer, J. (2005). Prospect theory and political science. Annual Review of Political Science, 8, 1–21.

Nguyen, Q. D., & Leung, P. (2009). Do fishermen have different attitudes toward risk? An application of prospect theory to the study of Vietnamese fishermen. Journal of Agricultural and Resource Economics, 34(3), 518–538.

Prelec, D. (1998). The probability weighting function. Econometrica, 66(3), 497–528.

Reynaud, A., & Couture, S. (2012). Stability of risk preference measures: Results from a field experiment on French farmers. Theory and Decision, 73(2), 203–221.

Schmidt, U., & Traub, S. (2002). An experimental test of loss aversion. Journal of Risk and Uncertainty, 25(3), 233–249.

Scholten, M., & Read, D. (2014). Prospect theory and the “forgotten’’ fourfold pattern of risk preferences. Journal of Risk and Uncertainty, 48(1), 67–83.

Slovic, P., & Lichtenstein, S. (1968). The relative importance of probabilities and payoffs in risk taking. Journal of Experimental Psychology, 78, 1–18.

Tanaka, T., Camerer, C. F., & Nguyen, Q. (2010). Risk and time preferences: Linking experimental and household survey data from Vietnam. American Economic Review, 100(1), 557–571.

Tversky, A., & Kahneman, D. (1992). Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty, 5(4), 297–323.

Wakker, P. P. (2010). Prospect theory: For risk and ambiguity. Cambridge: Cambridge University Press.

Wakker, P., & Deneffe, D. (1996). Eliciting von Neumann–Morgenstern utilities when probabilities are distorted or unknown. Management Science, 42(8), 1131–1150.

Wakker, P. P., Köbberling, V., & Schwieren, C. (2007). Prospect-theory’s diminishing sensitivity versus economic intrinsic utility of money: How the introduction of the Euro can be used to disentangle the two empirically. Theory and Decision, 63, 205–231.

Wehrung, D. A. (1989). Risk taking over gains and losses: A study of oil executives. Annals of Operations Research, 19, 115–139.

Zhao, S., & Yue, C. (2020). Risk preferences of commodity crop producers and specialty crop producers: An application of prospect theory. Agricultural Economics, 51, 359–372.

Acknowledgements

The authors thank Kene Boun My for help with the implementation of the experiment and Marie-Claire Villeval for useful advice for a previous version of the article.

Funding

This research was funded by the Contrat de plan État-région (CPER) Lorraine Ariane under the project RIM (Risques Industriels et Multiples). The UMR BETA is supported by a grant from the French National Research Agency (ANR) as part of the "Investissements d’Avenir" programme, Lab of Excellence ARBRE (Grant No. ANR-11-LABX-0002-01).

Author information

Authors and Affiliations

Contributions

All the authors contributed to the design of the experiment and preparation of the experimental material. Data collection was performed by JJ and MB. Data analysis was carried out by GB. The first draft of the manuscript was written by GB and all the authors commented on later versions of the manuscript. All the authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Conflict of interest

The authors have no relevant financial or non-financial interests to disclose.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Below is the link to the electronic supplementary material.

Appendices

Appendix A: Lotteries of the LLo treatment

See Table 13.

Appendix B: Calculation of the individual PT parameters according to frame

We distinguish parameters and functions between the gain and loss frames through index d (d is \(+\) in the gain frame, d is − in the loss frame).

1.1 B.1 Calculation of \(\sigma ^{d}\) and \(\gamma ^{d}\)

The following calculations are valid for Series 1 and 2.

1.1.1 B.1.1 Gain frame

Let \(A(x_A,p_A;y_A)\) be the LHS lottery and \(B^l(x_{B_{l}},p_B;y_B)\) the RHS lottery of row l (\(x_A,y_A,x_{B_{l}}\) and \(y_B\) are strictly positive \(\forall l\), and \(0<p_A<1\) and \(0<p_B<1\)). The lottery structure is such that only \(x_{B_{l}}\) varies over rows l, while the other lottery attributes remain similar. For a given subject, switching at row s means the following inequalities in terms of prospect value:

From Eq. (2), we know that the prospect value of any lottery (x, p; y) is \(v^d(y)+ \omega ^d(p) \cdot (v^d(x)-v^d(y))\) when \(xy \ge 0\) and \(|x| > |y|\). Equations (1) and (3) give the functional forms for the value and probability weighting functions, respectively. Thus, we obtain

1.1.2 B.1.2 Loss frame

Let \(C^l(x_{C_{l}},p_C;y_C)\) be the LHS lottery of row l and \(D(x_D,p_D;y_D)\) the RHS lottery (\(x_{C_{l}},y_C,x_D,\) and \(y_D\) are strictly negative \(\forall l\), and \(0<p_C<1\) and \(0<p_D<1\)). The lottery structure is such that only \(x_{C_{l}}\) varies over rows l. This time, switching at row s means

As \(xy \ge 0\) still, any lottery (x, p; y) has the same prospect value than in the previous section, i.e. \(v^d(y)+ \omega ^d(p) \cdot (v^d(x)-v^d(y))\) when \(|x| > |y|\). Equation (1) gives the specific value function for the loss domain \(v^d(x)=-\lambda (-x)^{\sigma ^d}\) \(\forall x<0\). Thus,

Simplifying by \(-\lambda\), we obtain

As \(x_{C_{l}}= -x_{B_{l}}\) , \(y_C= -y_B\), \(x_D= -x_A\), \(y_D= -y_A\), and \(p_D= p_A\), \(p_C= p_B\), we further obtain

We can see that (7) is equivalent to (5), meaning that a similar couple of switching points in Series 1 and 2 \((s_1,s_2)\) in the gain domain and in the loss domain leads to a similar couple of parameters\((\sigma ^d,\gamma ^d)\).

1.2 B.2 Calculation of \(\lambda\), \(\lambda _\mathrm{oppos}\), and \(\lambda _\mathrm{gen}\) conditionally to \(\sigma ^{d}\)

The following calculations are valid for Series 3 only, where lotteries mix positive and negative payoffs. We distinguish \(\sigma ^{d1}\) and \(\sigma ^{d2}\), depending on which type of payoff the parameter applies to: \(\sigma ^{d1}\) applies to gains while \(\sigma ^{d2}\) applies to losses.

1.2.1 B.2.1 Gain frame

Let \(A^l(x_{A_{l}},p;y_{A_{l}})\) be the LHS lottery and \(B^l(x_B,p;y_{B_{l}})\) the RHS lottery of row l (\(x_{A_{l}}\) and \(x_B\) are strictly positive \(\forall l\), while \(y_{A_{l}}\) and \(y_{B_{l}}\) are strictly negative \(\forall l\), and \(p=\frac{1}{2}\) ). The lottery structure is such that only \(x_B\) does not vary over rows. A subject switching at row s means

From Eq. (2), we know that the prospect value of any binary lottery (x, p; y) is \(\omega ^d(p) \cdot v^d(x) + \omega ^d(p)(1-p) \cdot v^d(y)\) when \(xy \le 0\). As \(p = \frac{1}{2}\) it simplifies to \(\omega ^d(\frac{1}{2}) \cdot (v^d(x)+v^d(y))\). We designate as \(\lambda _{12}\) the loss-aversion parameter, which is equivalent to \(\lambda\), \(\lambda _\mathrm{oppos}\) or \(\lambda _\mathrm{gen}\) depending on the hypotheses relative to \(\sigma ^{d1}\) and \(\sigma ^{d2}\). We obtain

Last, as \(y_{A_{l}}\) and \(y_{B_{l}}\) are negative payoffs such as \(|y_{A_{l}}|<|y_{B_{l}}|\), \(\sigma ^{d1} >0\), and \(\sigma ^{d2} >0\), we can write

Inequations (9) define the bound values of \(\lambda\) when \(\sigma ^{d1}=\sigma ^{d2}=\sigma ^{+}\), \(\lambda _\mathrm{oppos}\) when \(\sigma ^{d1}=\sigma ^{d2}=\sigma ^{-}\), and \(\lambda _\mathrm{gen}\) when \(\sigma ^{d1}=\sigma ^{+}\) and \(\sigma ^{d2}=\sigma ^{-}\).

1.2.2 B.2.2 Loss frame

Let \(C^l(x_C,p;y_{C_{l}})\) be the LHS lottery and \(D^l(x_{D_{l}},p;y_{D_{l}})\) the RHS lottery of row l (\(x_C\) and \(x_{D_{l}}\) are strictly negative \(\forall l\), while \(y_{C_{l}}\) and \(y_{D_{l}}\) are strictly positive \(\forall l\), and \(p=\frac{1}{2}\) ). The lottery structure is such that only \(x_C\) does not vary over rows. A subject switching at row s means

As \(xy \le 0\) still, any lottery (x, p; y) has the same prospect value than in the previous section, i.e. \(\omega ^d(\frac{1}{2}) \cdot (v^d(x)+v^d(y))\). Equation (1) gives the specific value function for the loss domain \(v^d(x)=-\lambda _{12}(-x)^{\sigma ^d}\) \(\forall x<0\). We obtain

Last, as \(x_{C}\) and \(x_{D_{l}}\) are negative payoffs such as \(|x_{C}|>|x_{D_{l}}|\), \(\sigma ^{d1} >0\), and \(\sigma ^{d2} >0\), we can write:

As \(x_C = -x_B\) , \(y_C = -y_B\), \(x_D = -x_A\) and \(y_D = -y_A\), then Eq. (11) can be written as

Inequations (12) define the bound values of \(\lambda\) when \(\sigma ^{d1}=\sigma ^{d2}=\sigma ^{-}\), \(\lambda _\mathrm{oppos}\) when \(\sigma ^{d1}=\sigma ^{d2}=\sigma ^{+}\), and \(\lambda _\mathrm{gen}\) when \(\sigma ^{d1}=\sigma ^{+}\) and \(\sigma ^{d2}=\sigma ^{-}\).

As a last remark, in the special case when \(\sigma ^{d1}=\sigma ^{d2}\), note that the bound values of the loss-aversion parameter in the gain and in the loss frames are linked. Recall that, in the gain frame, the bounds of the loss-aversion parameter are (Eq. (9)):

Comparing with Eq. (12) provides the following equivalencies for \(\lambda\) bounds, which also apply to \(\lambda _\mathrm{oppos}\):

Appendix C: Raw results

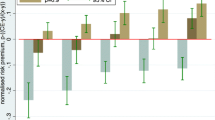

Appendix D: Comparison of PT parameter values from various studies

See Fig. 1.

Mean parameter values from studies using the TCN methodology

Appendix E: Alternative regressions

Appendix F: Distribution of individual PT parameter values

Distribution of individual PT parameters for baseline treatment GLo

Distribution of individual \(\sigma ^d\) parameters over treatments

Distribution of individual \(\gamma ^d\) parameters over treatments

Distribution of individual \(\lambda\) parameters over treatments

Appendix G: Distribution of selected individual loss-aversion values

Distribution of individual \(\lambda\) values in baseline GLo and \(\lambda _\mathrm{oppos}\) values in treatment LLo

Distribution of individual \(\lambda\) values in treatment GHi and \(\lambda _\mathrm{oppos}\) values in treatment LHi

Rights and permissions

Springer Nature or its licensor holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Bocquého, G., Jacob, J. & Brunette, M. Prospect theory in multiple price list experiments: further insights on behaviour in the loss domain. Theory Decis 94, 593–636 (2023). https://doi.org/10.1007/s11238-022-09902-y

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11238-022-09902-y